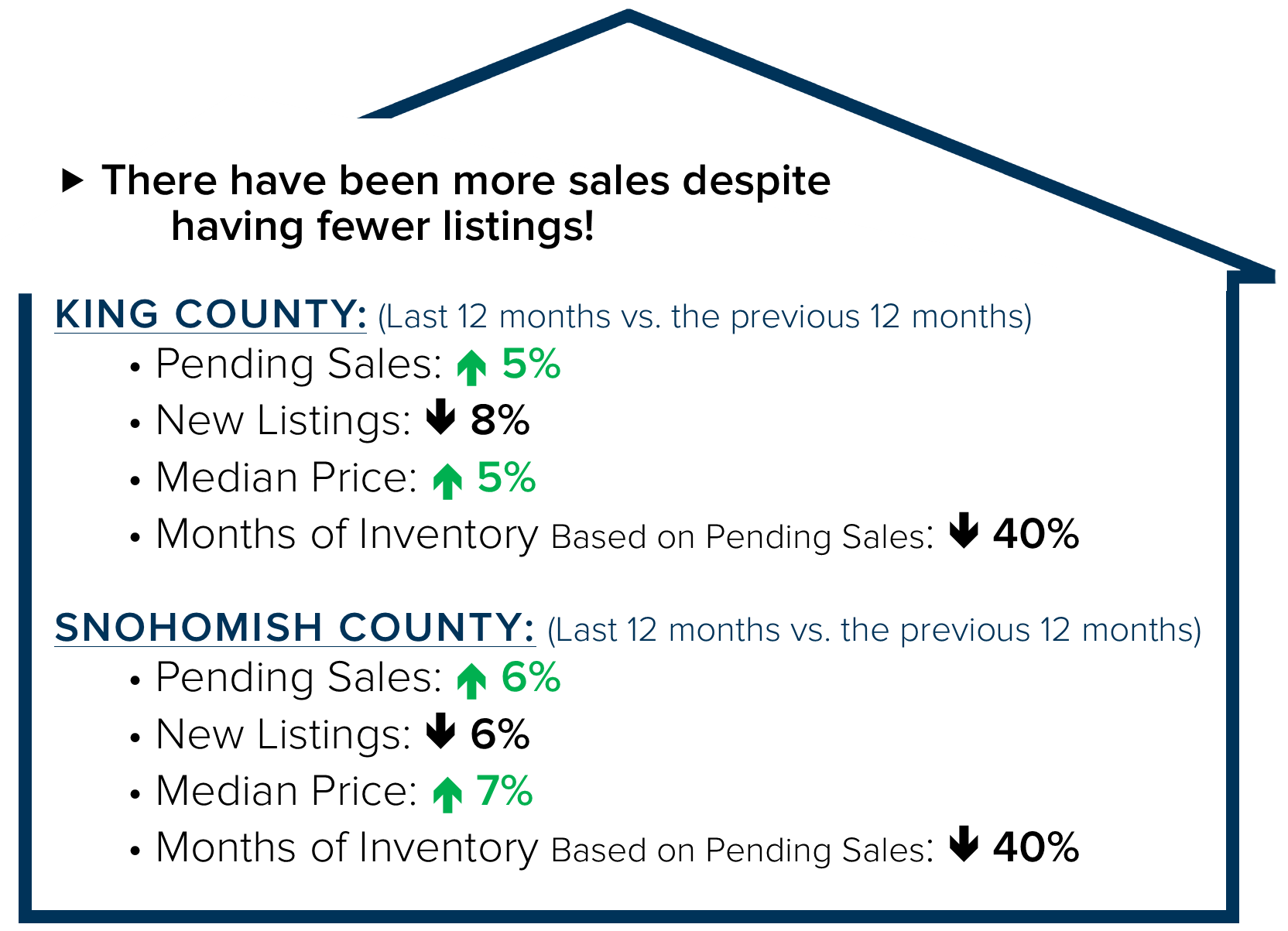

The real estate market continued to positively perform in the third quarter, and is the bright light in the economy during the COVID-19 health crisis. The protocols in place that have helped protect the safety of the community have recently been expanded to allow small group open houses to help address the demand in the market.

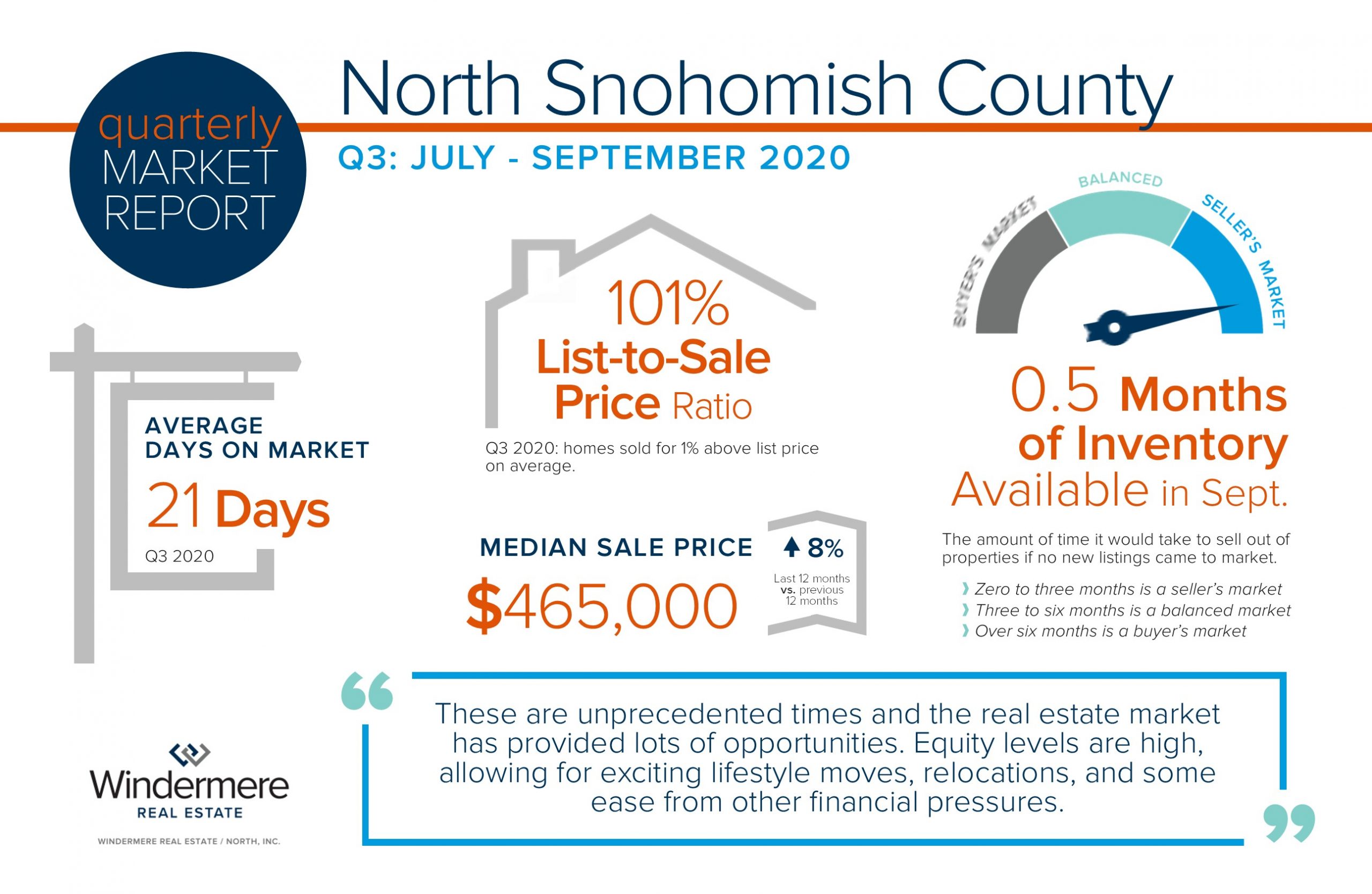

Interest rates remain historically low, hovering around 3% and creating robust buyer demand and a competitive marketplace. Coupled with available inventory being down 55% complete year-over-year, the third quarter saw many home sales escalate in price due to multiple offers. This perfect storm of supply and demand has amped up price appreciation. With only 0.5 months of available inventory based on pending sales, the median price is up 8% complete year-over-year.

Inventory is down due to the high absorption rate. There was a delay in homes coming to market in the spring, but the summer months finally caught us up with the previous year’s number of new listings. The influence of interest rates, along with many people making big lifestyle moves due to working from home, Baby Boomers retiring, and the younger generations transitioning their work and family statuses have resulted in 6% more sales complete year-over-year.

These are unprecedented times and the real estate market has provided lots of opportunities. Equity levels are high, allowing for exciting lifestyle moves, relocations, and some ease from other financial pressures. It is my goal to help keep my clients informed and empower strong decisions, now more than ever. Please reach out if you’d like to discuss your real estate goals and how they relate to your lifestyle and bottom line. Be well!

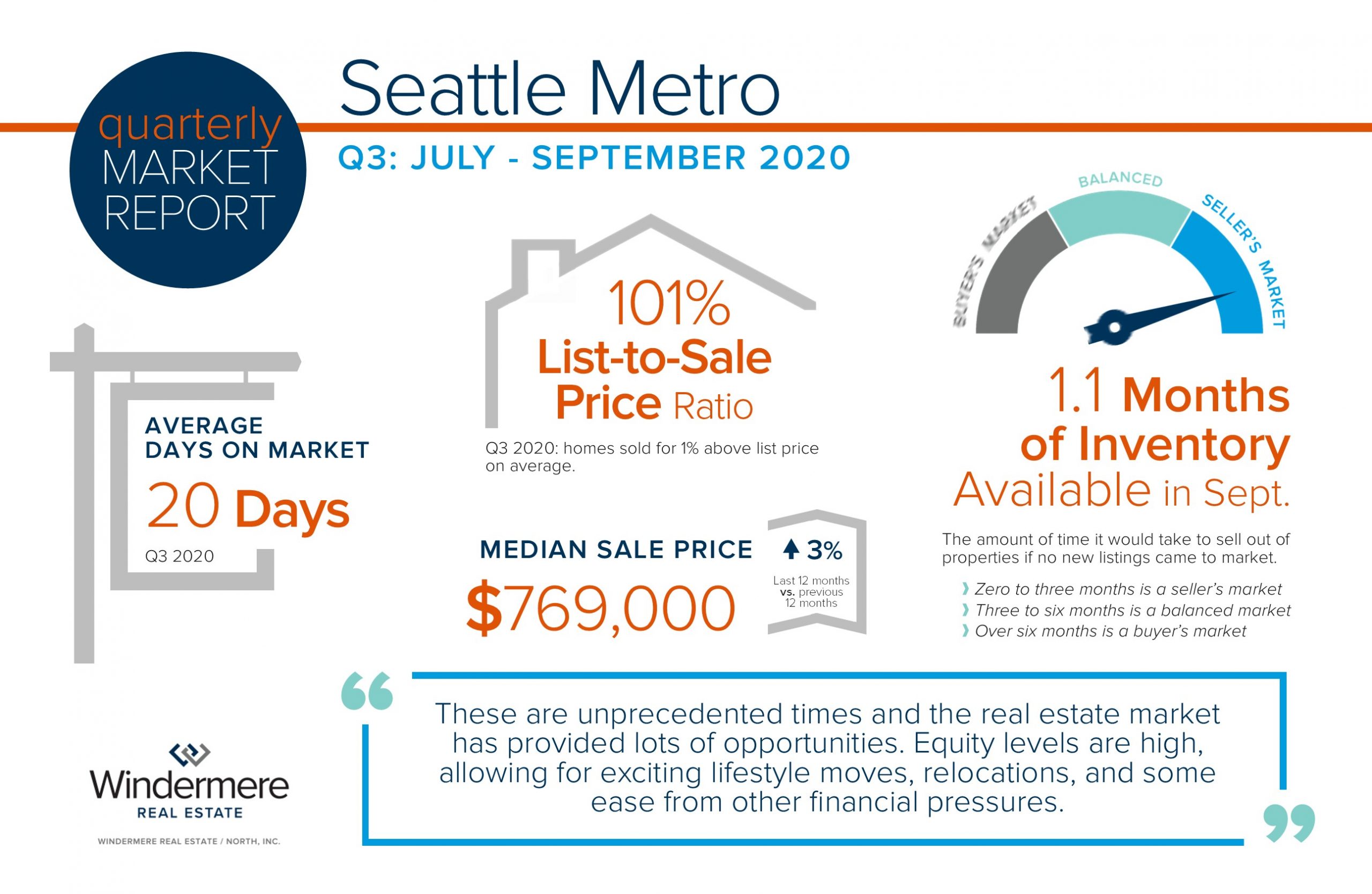

The real estate market continued to positively perform in the third quarter, and is the bright light in the economy during the COVID-19 health crisis. The protocols in place that have helped protect the safety of the community have recently been expanded to allow small group open houses to help address the demand in the market.

Interest rates remain historically low, hovering around 3% and creating robust buyer demand and a competitive marketplace. Coupled with available inventory being down 17% complete year-over-year, the third quarter saw many home sales escalate in price due to multiple offers. This perfect storm of supply and demand has maintained price appreciation. With only 1.1 months of available inventory based on pending sales, the median price is up 3% complete year-over-year.

Inventory is down due to the high absorption rate which resulted in many sales. There was a delay in homes coming to market in the spring, but the summer months got us equal with the previous year’s number of new listings. The influence of interest rates, along with many people making big lifestyle moves due to working from home, Baby Boomers retiring, and the younger generations transitioning their work and family statuses have resulted in 10% more sales complete year-over-year.

These are unprecedented times and the real estate market has provided lots of opportunities. Equity levels are high, allowing for exciting lifestyle moves, relocations, and some ease from other financial pressures. It is my goal to help keep my clients informed and empower strong decisions, now more than ever. Please reach out if you’d like to discuss your real estate goals and how they relate to your lifestyle and bottom line. Be well!

The real estate market continued to positively perform in the third quarter, and is the bright light in the economy during the COVID-19 health crisis. The protocols in place that have helped protect the safety of the community have recently been expanded to allow small group open houses to help address the demand in the market.

Interest rates remain historically low, hovering around 3% and creating robust buyer demand and a competitive marketplace. Coupled with available inventory being down 58% complete year-over-year, the third quarter saw many home sales escalate in price due to multiple offers. This perfect storm of supply and demand has amped up price appreciation. With only 0.6 months of available inventory based on pending sales, the median price is up 6% complete year-over-year.

Inventory is down due to the high absorption rate which resulted in many sales. There was a delay in homes coming to market in the spring, but the summer months got us within 12% of the previous year’s number of new listings. The influence of interest rates, along with many people making big lifestyle moves due to working from home, Baby Boomers retiring, and the younger generations transitioning their work and family statuses have resulted in only 4% fewer sales complete year-over-year.

These are unprecedented times and the real estate market has provided lots of opportunities. Equity levels are high, allowing for exciting lifestyle moves, relocations, and some ease from other financial pressures. It is my goal to help keep my clients informed and empower strong decisions, now more than ever. Please reach out if you’d like to discuss your real estate goals and how they relate to your lifestyle and bottom line. Be well!

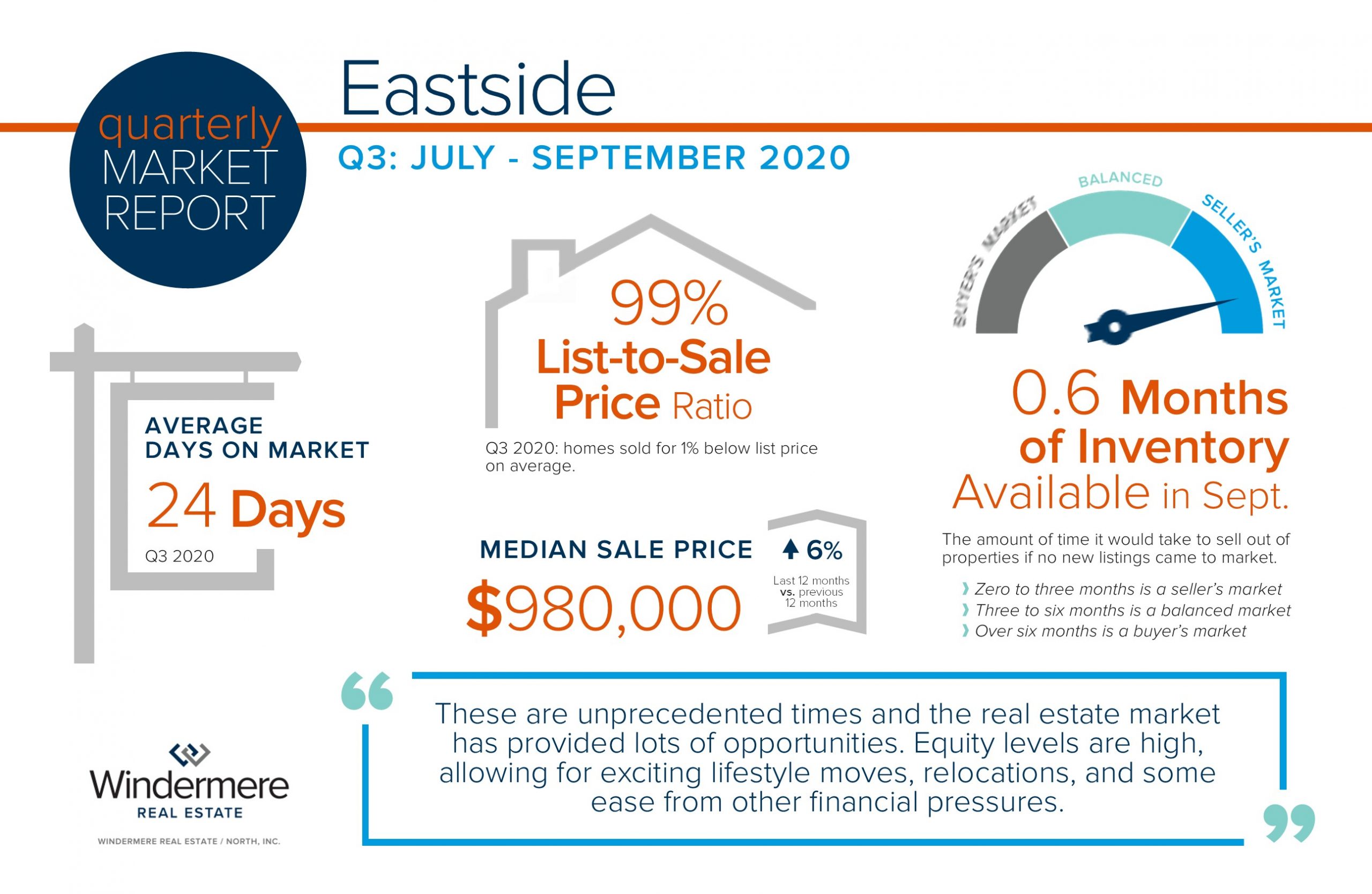

The real estate market continued to positively perform in the third quarter, and is the bright light in the economy during the COVID-19 health crisis. The protocols in place that have helped protect the safety of the community have recently been expanded to allow small group open houses to help address the demand in the market.

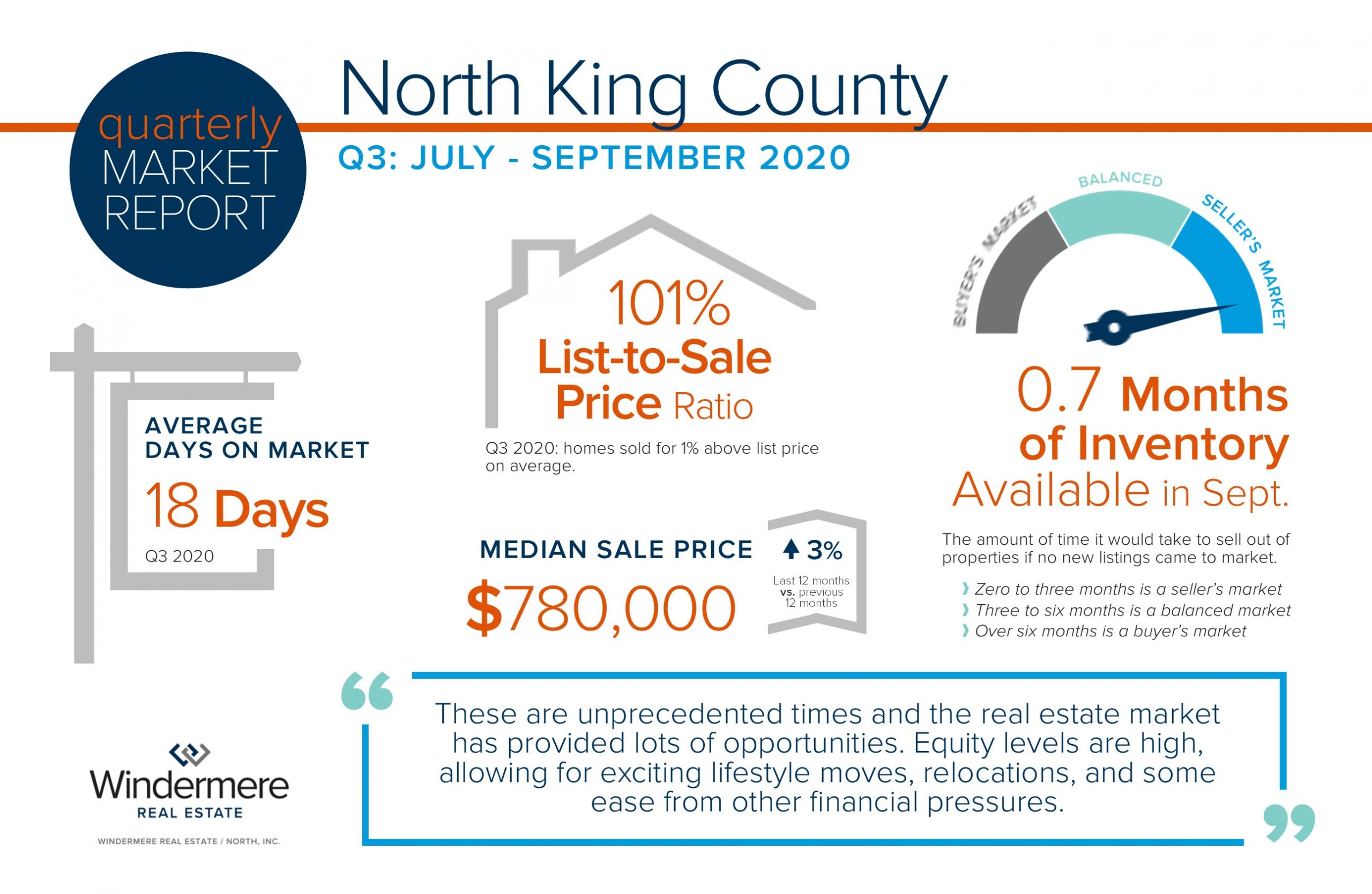

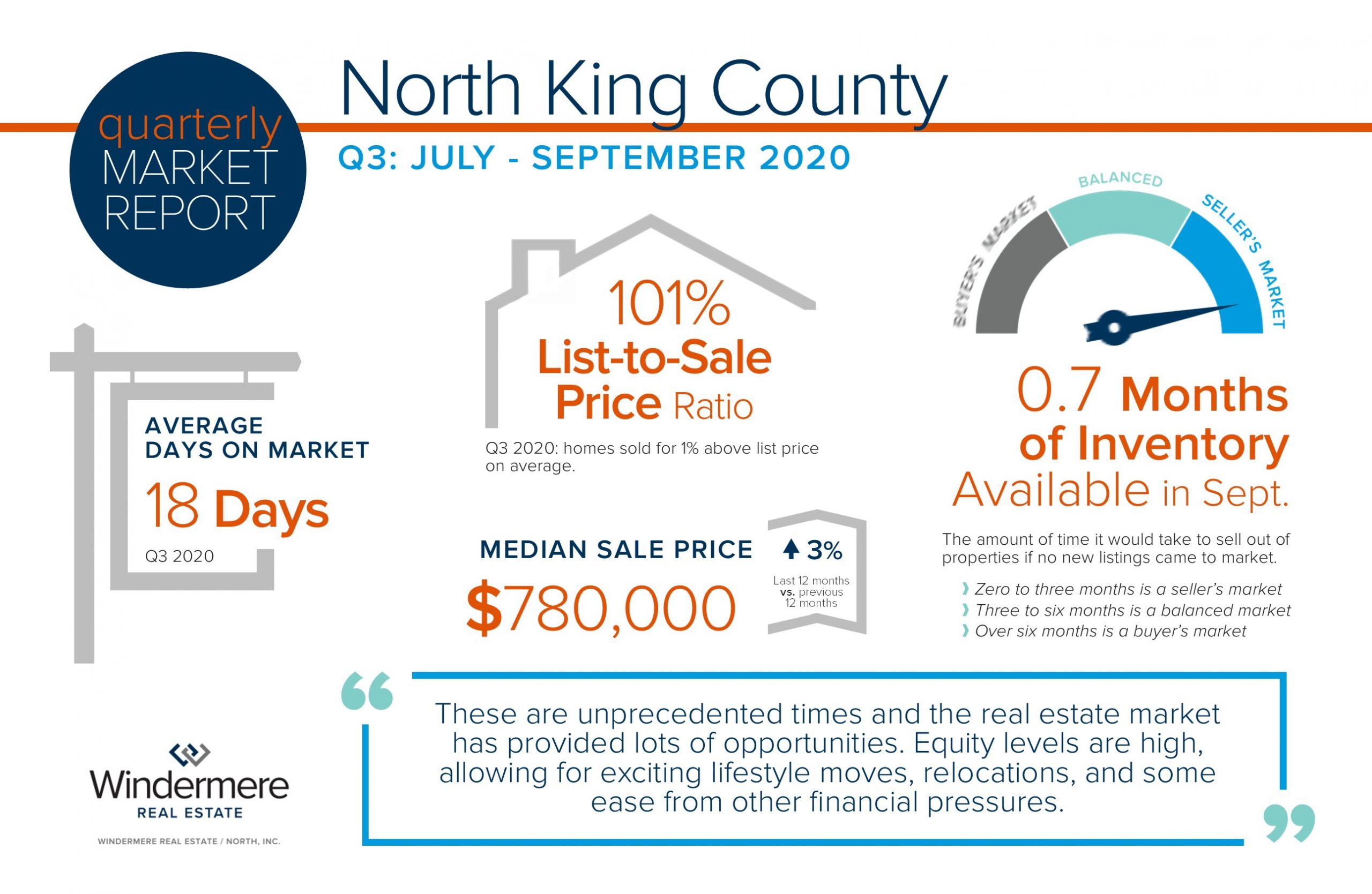

Interest rates remain historically low, hovering around 3% and creating robust buyer demand and a competitive marketplace. Coupled with available inventory being down 45% complete year-over-year, the third quarter saw many home sales escalate in price due to multiple offers. This perfect storm of supply and demand has maintained price appreciation. With only 0.7 months of available inventory based on pending sales, the median price is up 3% complete year-over-year.

Inventory is down due to the high absorption rate which resulted in many sales. There was a delay in homes coming to market in the spring, but the summer months got us within 6% of the previous year’s number of new listings. The influence of interest rates, along with many people making big lifestyle moves due to working from home, Baby Boomers retiring, and the younger generations transitioning their work and family statuses have resulted in 6% more sales complete year-over-year.

These are unprecedented times and the real estate market has provided lots of opportunities. Equity levels are high, allowing for exciting lifestyle moves, relocations, and some ease from other financial pressures. It is my goal to help keep my clients informed and empower strong decisions, now more than ever. Please reach out if you’d like to discuss your real estate goals and how they relate to your lifestyle and bottom line. Be well!

The real estate market continued to positively perform in the third quarter, and is the bright light in the economy during the COVID-19 health crisis. The protocols in place that have helped protect the safety of the community have recently been expanded to allow small group open houses to help address the demand in the market.

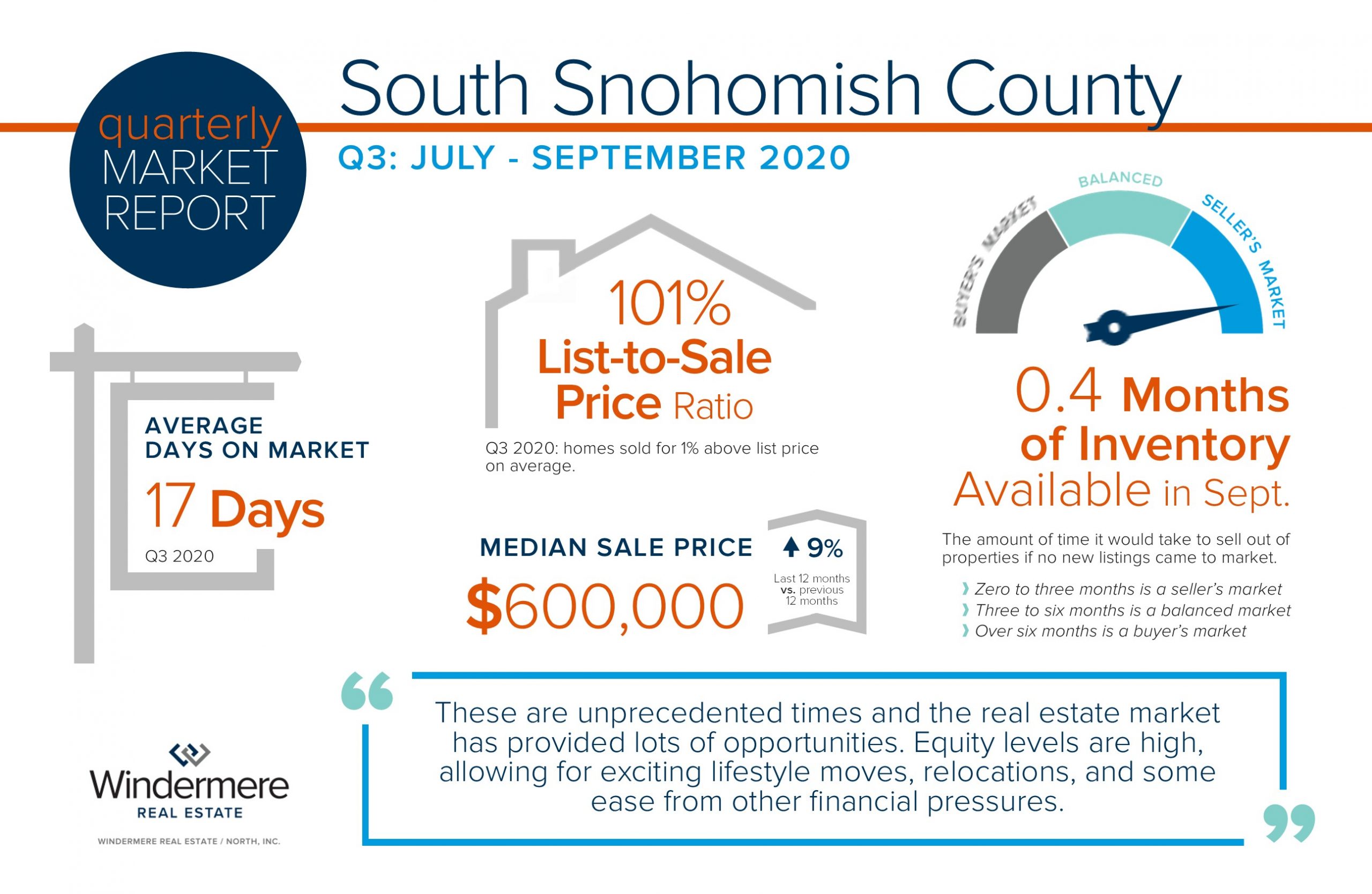

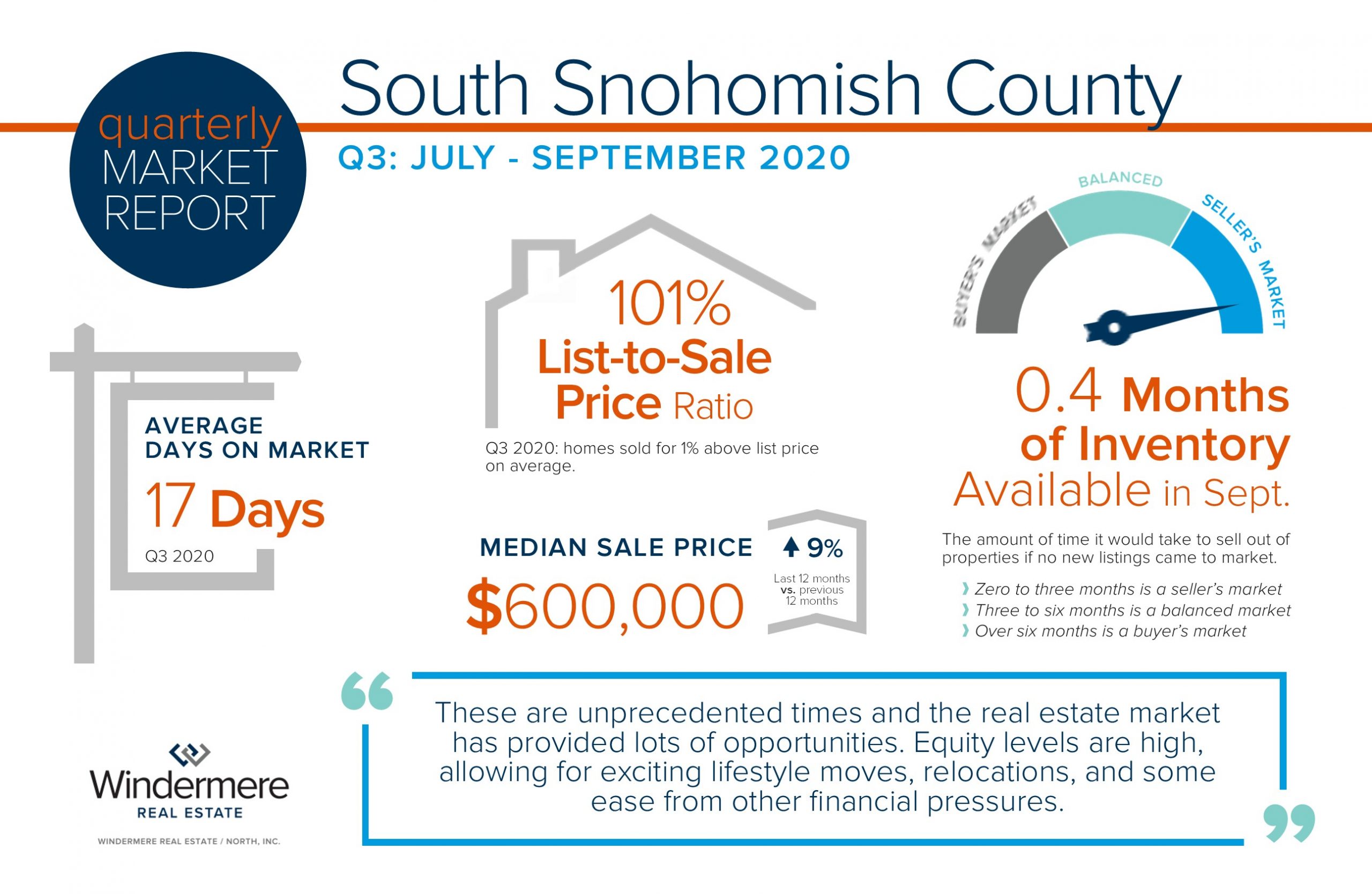

Interest rates remain historically low hovering around 3% and creating robust buyer demand and a competitive marketplace. Coupled with available inventory being down 72% complete year-over-year, the third quarter saw many home sales escalate in price due to multiple offers. This perfect storm of supply and demand has amped up price appreciation. With only 0.4 months of available inventory based on pending sales, the median price is up 9% complete year-over-year.

Inventory is down due to the high absorption rate which resulted in many sales. There was a delay in homes coming to market in the spring, but the summer months got us within 10% of the previous year’s number of new listings. The influence of interest rates, along with many people making big lifestyle moves due to working from home, Baby Boomers retiring, and the younger generations transitioning their work and family statuses have resulted in only 3% fewer sales complete year-over-year.

These are unprecedented times and the real estate market has provided lots of opportunities. Equity levels are high, allowing for exciting lifestyle moves, relocations, and some ease from other financial pressures. It is my goal to help keep my clients informed and empower strong decisions, now more than ever. Please reach out if you’d like to discuss your real estate goals and how they relate to your lifestyle and bottom line. Be well!

Homeowners across our region are enjoying very healthy equity levels due to an amazing upswing in the real estate market over the last five years. In fact, the median price in King County is up 49% over the last five years and up 51% in Snohomish County. This growth in equity has given homeowners the exciting option to sell their homes for a price that will bear a sizable down payment or the ability to “buy all-cash” on their next home. This has many people exploring their next chapters, such as moving up to a larger home or downsizing for retirement. The strong price appreciation is great news and provides many opportunities; however, we have also faced some challenges in how to make these transitions work without moving twice. Our biggest challenge for homebuyers in the marketplace right now is inventory levels. It is also the reason so many home sellers are doing so well. Currently, King County sits at 0.9 months of inventory based on pending sales and 0.6 months in Snohomish County. Historically, buyers that are also sellers would commonly secure a new home with a home sale contingency on the sale of their current home. Meaning the seller of the new home they are buying would give them a month or so to get their current house sold in order to be able to buy theirs. Well in this market, utilizing a home sale contingency is only rarely an option, especially on desirable homes. So, the million-dollar question is this: how does one who has gained so much equity, now itching to get that bigger house, different location, or perfect rambler for settling into retirement, make this transition without having to move twice? We need to get creative and have a strategy. The Windermere Bridge Loan program has been a powerful tool to help homebuyers transition their equity without having to sell their house first. This is an amazing tool for homeowners that own their homes free-and-clear or have gained a large amount of equity over time. This is also a low-cost and faster alternative to a cash-out re-fi or securing a HELOC which enables one to pull the equity out of their current house prior to selling it in order to make a non-contingent offer. The way it works is we take the market value of the house the homeowner current lives in, established by a comparative market analysis (CMA) that I complete and is approved by my Broker. We then take 75% of the CMA value and subtract any debt owed, and that is the maximum amount the homeowner can borrow for their next down payment. For example, if the market value is $700,000: 75% of $700,000 is $525,000. Say the homeowner owes a remaining $225,000 on their mortgage; the max amount they could borrow would be $525,000 – $225,000 = $300,000. If that same homeowner didn’t have a mortgage then they could borrow up to $525,000 as that is 75% of the CMA value. This tool enables people to make transitions without having to sell their home first, attempt a home-sale-contingent offer, or go through the lengthy and expensive process of a cash-out re-fi or securing a HELOC. What makes this tool so efficient, is that it doesn’t require an appraisal (like a re-fi or HELOC does), and these can easily be turned around in 5-7 business days. This tool provides the opportunity to quickly and inexpensively pull your equity out, be competitive, and eliminates the double move. The fees associated with this program are a 1% loan fee on the loan amount (minimum fee of $1,000), a title report, credit report, recording fees for the deed, and interest that is incurred between the loan funding and being paid off once the subject home is sold. That interest is conveniently wrapped up in the closing costs when the client closes the sale of the collateral home, eliminating the need to make monthly interest payments. Clients who use this program are also required to list the home 30 days after the loan has funded. This allows time for the client to prepare their home for sale after they have moved out. Lastly, only homes in Washington state are eligible to be the collateral property, but note this can be a tool for relocating out-of-state which we are seeing a lot of. In a strategy that is somewhat mind-blowing, we can sometimes use these bridge loans and never have to actually fund them. For example, if we secure a property non-contingent with the bridge loan and immediately get the subject home on the market, we can often secure a sale with a simultaneous closing, and never have to fund the loan. This eliminates the loan fee, interest, and the need to carry two mortgages. All this requires is getting pre-approved for the bridge loan and preparing the home for sale prior to shopping, so one is prepared to act quickly and line up both closings. If you are excited about equity levels and today’s low interest rates and have thought about making that move you’ve been waiting for, but have been fearful of how to do it all – I can help. The Windermere Bridge Loan, along with great attention to detail, hand-holding, and careful planning have helped many people make these exciting transitions. It is my goal to help keep my clients informed and empower strong decisions. Please contact me if you would like further information on how this might work for you or someone you know.

As the Official Real Estate company of the Seattle Seahawks, Windermere donates $100 to Mary’s Place for every home game Hawks tackle. During the last home game against the Cowboys we raised $5,300, bringing our total to $131,000. We’ll continue to #TackleHomelessness.

We’ve said it so many times, but it is so true: these are unprecedented times! In relation to the real estate market, there are many factors that are contributing to this environment. First and foremost, we are living through a global pandemic. Our daily lives have changed and they will probably never be quite like they were before. Besides this major upheaval in life as we know it, we have the lowest interest rates ever in history (this won’t last forever), formidable equity levels, and we are at the corner of a generational shift. These factors are fueling demand in the real estate market despite the challenges the pandemic has brought to light. In fact, the pandemic has influenced some very big lifestyle moves due to having time to reflect on goals and the new normal of working remotely. Low interest rates, Baby Boomers retiring, Millennials stepping up to the home-ownership plate, Gen X settling into their forever homes, and commute times becoming less important are the ingredients in the proverbial pot that is being stirred in the 2020 real estate market. The demand is high! Couple that with a reduction in new listings over the last year and it is competitive. Sellers are in such a favorable position and buyers are devising solid plans to win a home with the lowest debt service in history. Before I share some tips on how to win a home in today’s market, let’s look at the numbers. 2020 started off with abnormally low inventory levels following 2019 when we were headed toward more balance in the marketplace. Then COVID hit and the market briefly stalled. There were 8 weeks in King County and 4 weeks in Snohomish County from the onset of COVID where the market performed under 80% of the pending sales rate in 2019. We adjusted rather quickly as the influence of the demand mentioned above found its way with masks on and hand sanitizer at the ready.

Now that we have established that the demand is strong, debt service is low, and that lifestyle moves are leading the way, how do you make it happen if you want to participate? Partner with a Broker Who Will Get the Job Done A broker that has a process is key!It starts with an initial buyer consultation.I liken the buyer consultation to the seat belt you would wear on a roller coaster. The buyer consultation aims to unearth a buyer’s goals, research the areas they are interested in, address financing, and illustrate the challenges of the environment, so one can be successful.Time is money, and this consultation brings clarity, efficiency, and trust. This upfront education coupled with a high level of communication and availability is paramount.The depth of the relationship will lead to success and is the ingredient that enables a buyer to throw up their hands and take the thrilling plunge on the roller coaster.It is hard to do that without a seat belt! Get Your Finances in Order Aligning with a trusted real estate professional is key, but so is aligning with a reputable and responsive mortgage lender.Getting pre-approved is the minimum, but getting pre-underwritten is a game-changer. Finding a lender that is willing to put in the work up-front to vet credit, income, savings, debt, and all other financial indicators will lead to being pre-underwritten, which listing agents and sellers appreciate!Also, be aware that you do not always need to have a huge down payment to make a purchase work.Employment, assets, credit, and what you have saved all work into your ability to acquire a loan.I have seen plenty of people secure a home with 3-5% down.Education and awareness create clarity, and investing into understanding your financial footing equals empowered and more efficient decisions.Note that I mentioned “responsive”. This is a 24/7 market, and lenders who don’t work evenings and weekends can get in the way of a buyer securing a home.If you need a shortlist of lenders that fit this description, please contact me. Be Willing to Take Calculated Risks Buyer due diligence is key to making a sound investment. Even though timelines are tight and buyers must act swiftly, it is not time to just throw caution to the wind. Having some funds set aside to perform a pre-inspection will help a buyer make a purchase with both eyes open and be competitive. Also, going back to getting pre-underwritten, this could empower a buyer to waive financing and beat out all-cash buyers. Strategizing Down Payment Funds Many buyers are moving big chunks of equity from their previous home to the one they are buying. Equity levels are deep and prevailing buyers are commonly reserving some of their equity to offset appraisal risk for a seller. The market is appreciating so rapidly that a buyer holding back down payment funds and shifting them to an appraisal safety net has been one of the most successful strategies to help a buyer win a home. The best part is the safety net only seldomly has to be used. This plays into the calculated risk category and also highlights the importance of a good lender and broker to help navigate such decisions. The Triangle of Buyer Clarity Buyers must be realistic with their expectations. The triangle of buyer clarity rests on the three corners of Location, Price, and Condition. If a buyer continues to run into walls when making offers it typically has to do with the need to adjust one of the corners of the triangle. Buying a home take compromise, especially with such low inventory. By staying connected to the big picture of building wealth with low debt service, gaining a home that will work with your goals may require an adjustment of location, price, or level of condition. Focusing on the triangle of buyer clarity and talking it through during the buying process leads to clarity and success. A rule of thumb to bear in mind is that when a home starts to check 75% of your boxes, it should be considered. The 2020 real estate market has provided a ton of opportunity during a very challenging time. It’s been a bright light in the economy. If you are curious about how the current market relates to your housing and financial goals, please reach out. It is always my goal to help keep my clients informed so they are empowered to make strong decisions. Be well!

We are proud to be the official real estate company of the Seattle Seahawks! The best part of this partnership is our #TackleHomelessness campaign. For every home-game tackle the Hawks make, the Windermere Foundation donates $100 to Mary’s Place which provides safe, inclusive shelter and services supporting women, children and families on their journey out of homelessness. Go Hawks!

Nothing feels more like fall than pumpkin picking, hay rides and corn mazes. Get your latte in hand and head out to any one of these great, local farms to have some harvest fun and find that perfect jack-o-lantern to light up your porch.

Please be sure to verify and take note of each farm’s COVID-19 safety guidelines, as well as any potential weather-related (or COVID-related) closures or changes.

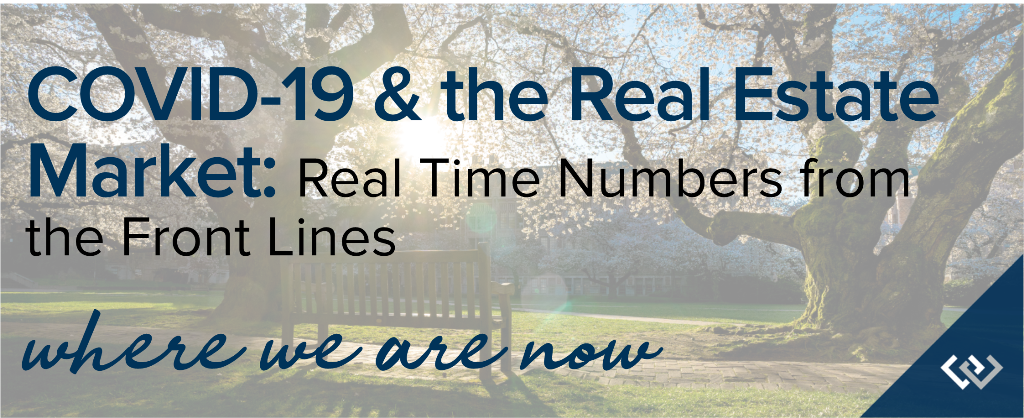

Over the last 5 years, housing has had abundant price appreciation, providing substantial equity for homeowners to utilize to make meaningful lifestyle moves or invest back into where they are. In King County, the median price has appreciated from $463,000 to $689,000 since July 2015, which is a 49% increase equaling $226,000! In Snohomish County, the median price has appreciated from $340,000 to $515,000 since July 2015, which is a 51% increase equaling $175,000. Bring on a global pandemic that has turned the world as we know it on its heels and the needs and desires for housing are starting to change! Solid equity positions and the changes brought on by the pandemic are creating The Big American Move. In a July survey by Realtor.com the results show that consumers are looking for larger interior spaces, more spacious outdoor areas, and a desire to move to suburban areas from urban locations. This has been fueled by the ability to work remotely, providing many homeowners the opportunity to pivot to locations not driven by commute times, but by the overall enjoyment of the spaces that the home and yard provide. In fact in that same survey, 2 out of 3 consumers noted the ability to work remotely was fueling their decision to move. Some are fleeing from urban density to more wide-open spaces to provide more room to roam for children as on-line school looked to be the plan for 2020-21. The pandemic has also spurred retirement for many, as well as adding the big retirement or second-home move to the east of the mountains or out of state. These markets are much more affordable, and folks that spent many years in their homes in King and Snohomish Counties are selling and turning their big chunks of equity into their dream oasis in the mountains, by the beach, or in the desert. Many of these purchases are able to be made all-cash due to the affordability of these areas in relation to liquidated equity. This simplifies life with no mortgage payments to maintain. An agent in my office just shared that of the last ten listings she had, eight either went east or out of state. The established equity, increased demand, low inventory, and the lowest interest rates we have ever seen have created one of the most vital housing markets ever. According to Housing Wire, the rebound in the housing market since the National Emergency was announced has been shockingly strong. Meyers Research calls it nothing short of remarkable. Home purchase mortgage applications are up year-over-year for 11 straight weeks since mid-May. Seven out of nine economists predict national price growth in 2020. Locally, Windermere’s Chief Economist Matthew Gardner predicts 5% year-over-year appreciation. In July, King County’s median price for Single Family Residential Homes (SFR) is up 3% complete year-over-year and Snohomish County (SFR) 6%. The higher price growth in Snohomish County is a reflection of the push to the suburbs and affordability. John Burns Consulting is calling this The Great American Move. The phenomenon is being fueled by safety reasons, financial prospects, life-change improvements, personal comfort, and employment. They expect a surge in household and business relocations over the next few months that will provide new, strategic opportunities for the real estate market. The Greater Seattle job market is still strong in many sectors and commutes will come back. While folks are cashing out their equity and going for larger spaces because they can, the Millennial generation is still very much attracted to the in-city neighborhoods. We have not seen this wealth transfer hurt these markets, as it is perfect timing for the maturing Millennials to put roots down in urban locations as they flourish in their careers, migrate to our area for work, marry, or start families.

2020 has been downright astonishing in regards to the housing market. In fact, it has felt like two different worlds managing the pace of such a brisk real estate market during a time where we have slowed down and simplified our daily lives. Maintaining the safety of everyone around me by observing all the proper safety protocols has been a top priority. I’ve felt a great responsibility to help my clients navigate some very big lifestyle decisions through the purchase and sale of their real estate. It has been an honor and something I take very seriously. It is always my goal to help keep my clients informed and to empower strong decisions, especially during this unprecedented time. Please reach out if you’d like me to answer any questions or shed light on the trends in your area. Be safe, be well!

Here we are again, with a new school year right around the corner. We all know that this year won’t be anything like what we’re used to, or what we hoped for… those fresh supplies, cute outfits, and all the “first day of school” pictures spamming our Facebook feed. Your family might be mourning what should have been, or you might be stressed just thinking about how you’re ever going to manage it all. Regardless of the initial opening decision your school has made, or what you have decided is best for your family, there is a lot of uncertainty ahead of us this fall and winter.

Below are a collection of tips and strategies I’ve put together for making the most (or maybe just surviving) this coming school year. It won’t look like a “normal” fall, but maybe we can still make it a good one.

1) Plan a daily routine

Take the time before the year begins to plan out a daily schedule and family routine. It is tempting to let everyone sleep in as much as possible and log into their Zoom sessions from bed, but it won’t be the best scenario for truly learning or engaging. Having structure and goals to work towards will set up your students for success and give them a sense of security and predictability.

2) Verify Materials

Make sure you have everything your kids will need to be successful. Your supply list this year might be fewer pens and markers and folders, and more along the lines of a PDF reader, note-taking apps, noise-canceling headphones, a stable WiFi connection, and pertinent account log-in information.

You might also think about purchasing some of those fresh, fun supplies, even if you won’t really need them. Maintaining a sense of normalcy will be important for everyone’s sanity. Some fun or pretty things for the kids to start the year with might go a long way for keeping their spirits up.

3) Create a Learning Environment

Everyone knows the learning environment is important. A space too isolated could create opportunity to slack off. Sitting at the kitchen table might prove to be too distracting. Really think about what each person’s needs are and be prepared to move or switch things around if you find something isn’t working well.

When creating everyone’s work space, think about distractions, comfort, and access to power. Try to eliminate distractions as much as possible. Background noise or music can help with concentration. Help your child create a playlist of soothing music, or try an app like this one for productivity and focus.

4) Plan Each Day

This is not the same as your family routine or school schedule. Help your student to make a plan for each day by taking a few minutes every morning to look at their schedule and assignments, and create a specific plan for that specific day. This will be especially helpful for older kids who might have lots of projects to juggle and independent work that can easily lead to feeling overwhelmed.

5) Center the Child, Not the Work

This may not be for every household, as it’s definitely more of a parenting philosophy. Some families may find it much more important during this uncertain time to prioritize working hard, rather than getting good grades. If nothing else, keep in mind that we are in unprecedented times, and everyone deserves some grace as we move through this. Our children included.

6) Encourage a Growth Mindset

A growth mindset doesn’t put the focus on what they’re learning in school, but rather how to think about what they’re learning. Developing a growth mindset will help your student reframe how they approach challenges in every aspect of their life. Kids with a growth mindset believe that their abilities, intelligence, and performance can improve over time. It’s the subtle difference between “I can’t do this homework. I don’t understand science.” and “I can’t do this homework yet. I don’t understand how to make sense of this problem.” Students with growth mindset see mistakes as ways to learn and will persist in the face of setbacks. We all need more of this, pandemic or not.

7) Mask Prep

Even if your school is 100% remote learning for the beginning of the year, we should be preparing our kids now for the possibility of a hybrid learning model that will hopefully come later in the school year. Most of us are familiar by now with wearing masks to the grocery store or in the park, but those situations are not the same as wearing a mask for 7 hours straight during a school day. Start preparing your student now for extended mask wearing.

Make sure you have several masks that properly fit your child.

Practice is key. Don’t expect perfection at first, especially with younger kids. Just know that the more they wear masks, the more comfortable they will feel. Practicing at home gives them a safe space to take it off when they need a break.

Build endurance. Start small, the way you would with any new habit. Have them wear the mask for small increments of time, and gradually build up.

Make it fun. Do fun activities while they have it on. Let them pick out the colors or the fabric, or buy plain ones along with fabric paint and let them design their own. Disposable masks can be personalized with stickers around the edges. Help them enjoy wearing the mask by letting it reflect their personality.

Explain the “why”. Children need to know why they have to wear the mask. Talk to them about germs and how the mask helps to prevent spreading sickness. Have lots of conversations with your teens and middle-school kids so they are armed with facts and information in case they experience peer pressure to stop wearing it.

Model what you want your kids to imitate. When you are asking your child to wear a mask, you should wear it along with them, even around the home when they are practicing.

8) Exercise Daily

This might get difficult when the winter weather sets in, but it is so important that we are all exercising every day. Even just a 30 minute walk does wonders for our bodies and our minds. Physical activity will make your student feel better, function better, learn better, and sleep better. It will reduce anxiety and improve overall health. Make this one a priority!

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link