Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

The question that many potential buyers are asking themselves right now is: should I wait for rates to drop before I buy? Higher interest rates have certainly made monthly payments higher and challenged overall affordability, however it is important to consider creative financing options and what the impact on prices will be once rates lower.

The question that many potential buyers are asking themselves right now is: should I wait for rates to drop before I buy? Higher interest rates have certainly made monthly payments higher and challenged overall affordability, however it is important to consider creative financing options and what the impact on prices will be once rates lower.

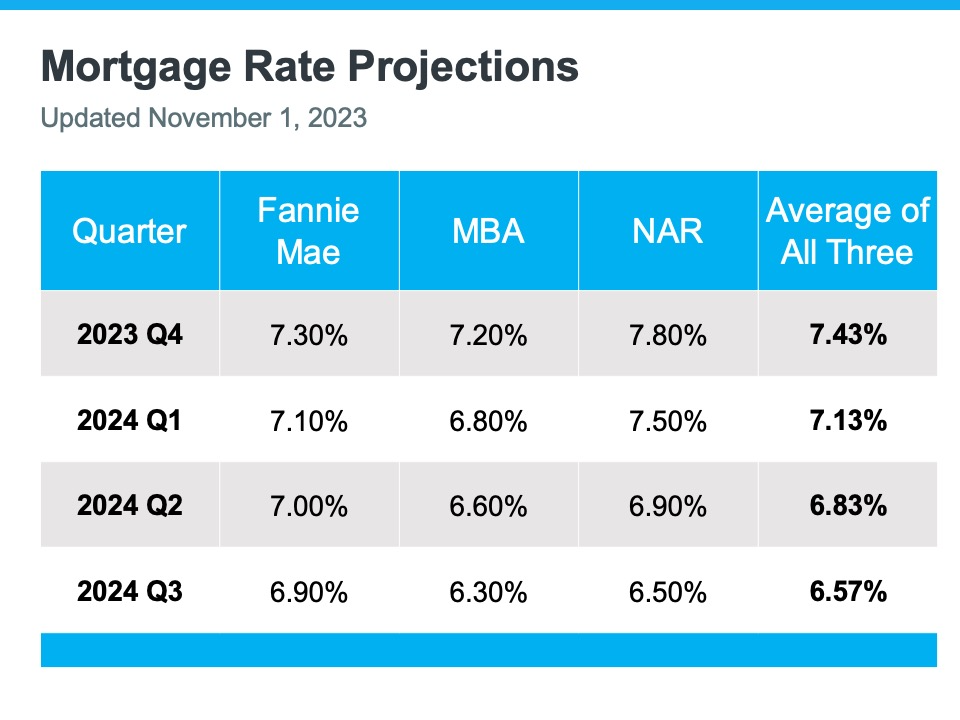

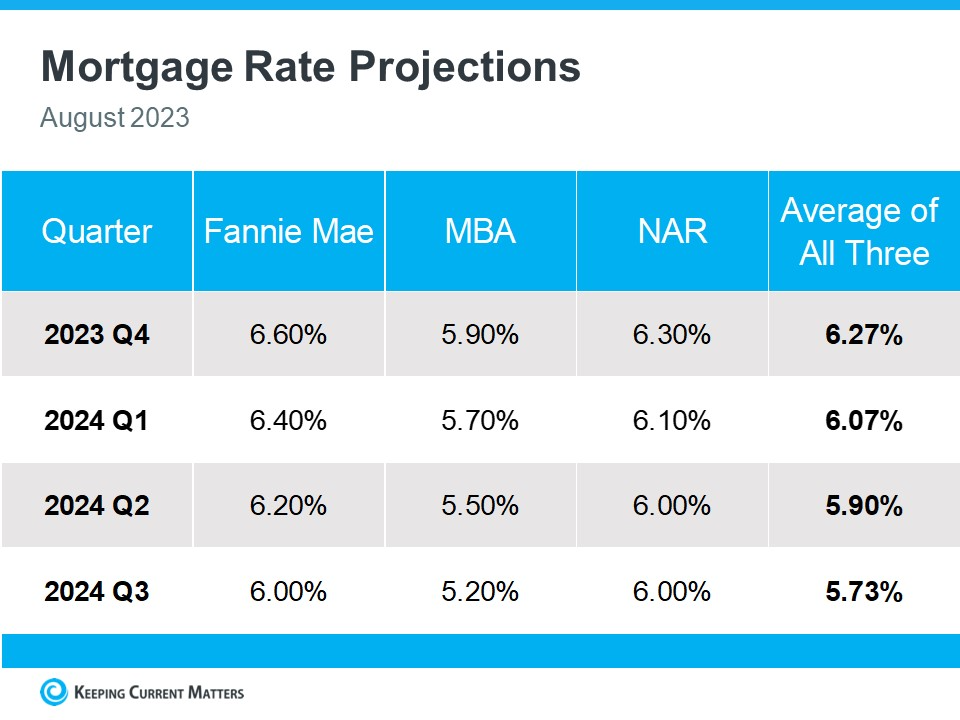

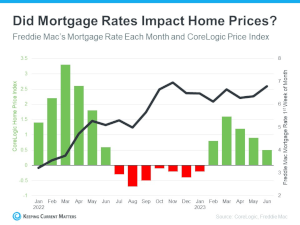

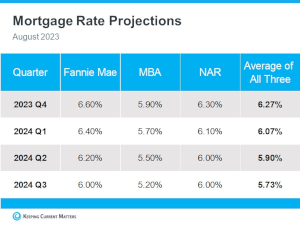

Experts predict rates to decrease over the next 12-18 months. In fact, we have seen rates drop half a point over the last 30 days. Currently, the 30-year conventional rate is hovering about 7.5%. We saw a correction in prices when rates jumped by a point and crested 6% in mid-2022. Since Dec 2022, prices found their bottom, and price appreciation started happening again. Year-to-date, the average interest rate has been around 7% and prices have not been in a free fall, they have grown and remain stable.

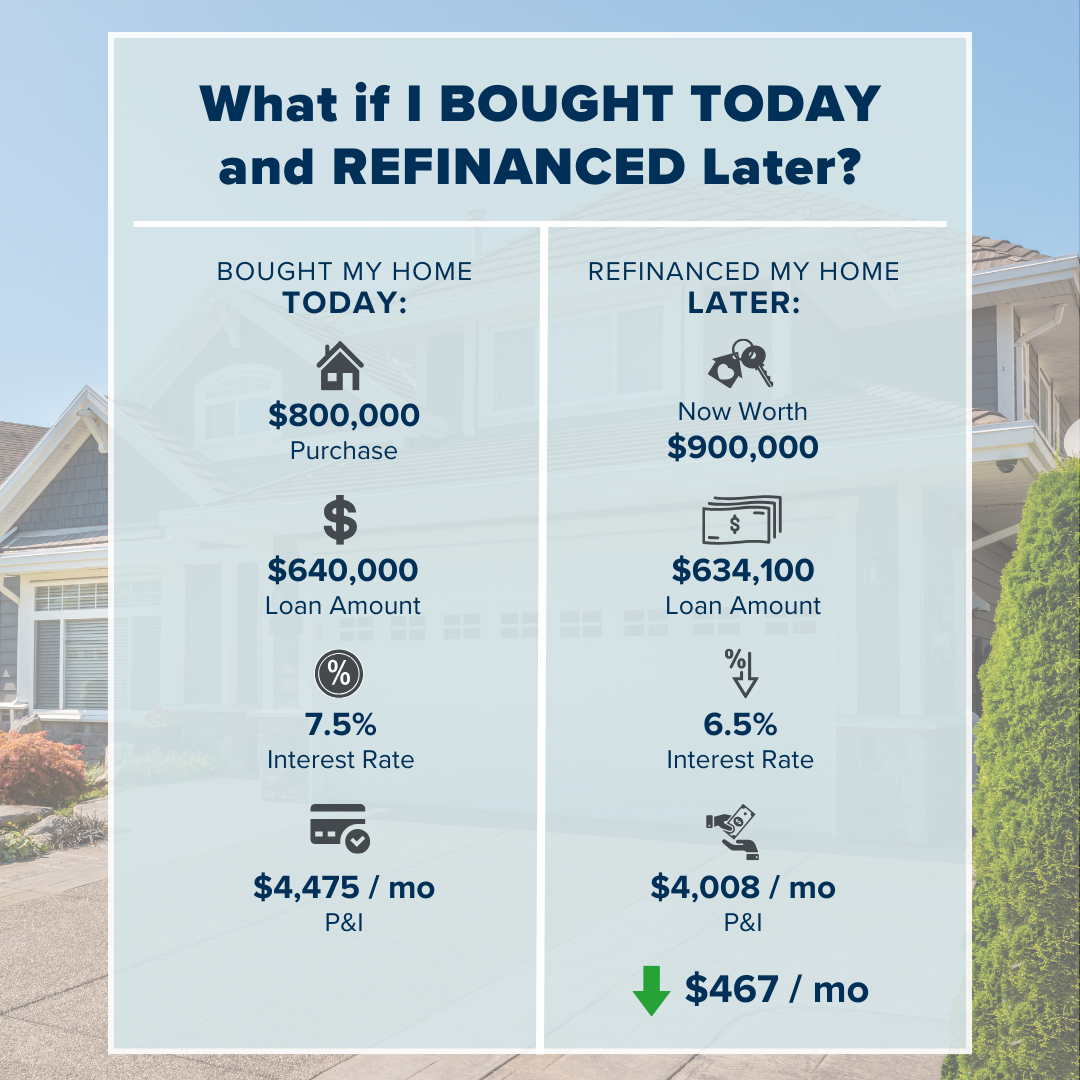

Just like the correction that happened in 2022, it is safe to say there is a correlation between prices and rates. If the experts are correct and rates fall over the course of the next year or so, we should anticipate prices to increase. That is what hangs in the balance when making the decision of whether to buy now or later. The example to the right shows the effect that price appreciation will have despite rates being lower. It was not that long ago that we were experiencing bidding wars where homes escalated in the double digits. As you can see, the higher price results in a higher payment even with the lower rate.

If one is able to afford a purchase now with today’s rate, they can refinance when rates go down and save themselves a lot of money on their payment while keeping a fixed price. Additionally, if a buyer can secure a rate buydown, such as a 2-1 buydown, the higher rates can be overcome and a refinance can fix the rate when the rates drop.

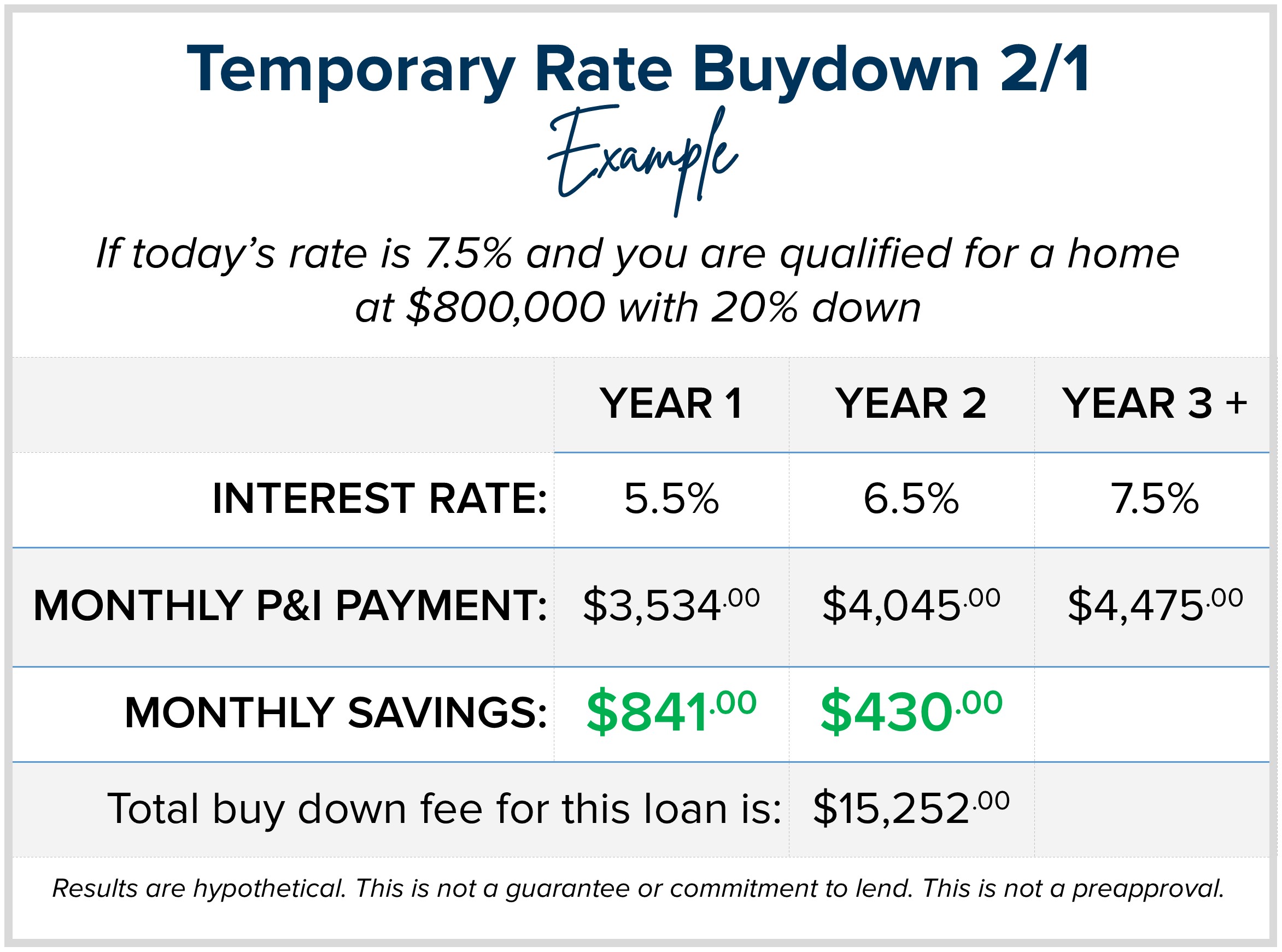

Here is an example: let’s say you are shopping for a house and have the same $800,000 budget and a 20% down payment with today’s rate of 7.5%. The monthly principal and interest payment would be $4,475.00. You could do a 2-1 buydown (2-points lower in year one and 1-point lower in year 2) which would have your payment in year one be based on an interest rate of 5.5% with a monthly principal and interest payment of $3,534 – a savings of $841.00 per month. For year two, the monthly principal and interest would be based on 6.5% resulting in a monthly payment of $4.045.00, a $430.00 per month savings. The total savings in monthly payments with the 2-1 buy-down over the two years would be $15,252.00.

The roughly $15,000 in monthly payment savings is paid upfront at closing and in some cases paid by the seller. The buyer still needs to qualify based on the 7.5% interest rate as the payments will convert to the payment based on the 7.5% in year three moving forward. The strategy here is to never have the payment increase to 7.5% because the buyer plans to refinance when rates come down, and will permanently fix their rate below 7.5%. A bonus is that if the entire $15,000 credit has not been used yet, in some cases those funds can be applied towards the refinance.

You see, there are many options to consider when a buyer is balancing rates, prices, payments, and their desire to make a move. I understand that I am in the business of helping people navigate big life changes while ensuring their financial investment is sound. I felt it was an important message to share these examples in case you or someone you know was thinking about making a purchase but was feeling confused or stifled by the current rate environment. If you want to learn more or need a referral to a reputable lender, please reach out. It is always my goal to help keep my clients well-informed and empower strong decisions.

As we approach the Thanksgiving holiday, I want to let you know how grateful I am for YOU! Your friendship, support, and referrals have helped fuel my business and support my family. Thank you!

Real estate is a career that gives me the opportunity to be a meaningful part of my clients’ lives as they navigate important moves that have a great financial impact. I take the responsibility of guiding my clients through this process very seriously and know that when someone places this trust in me that it is a big deal! It is an honor to be a part of your big-picture planning and to help you execute these life changes with care and success.

My Thanksgiving would not be complete without taking a moment to say thank you and that I appreciate you so much! I hope your holiday is filled with happiness, rest, and all the people that are nearest and dearest to your heart.

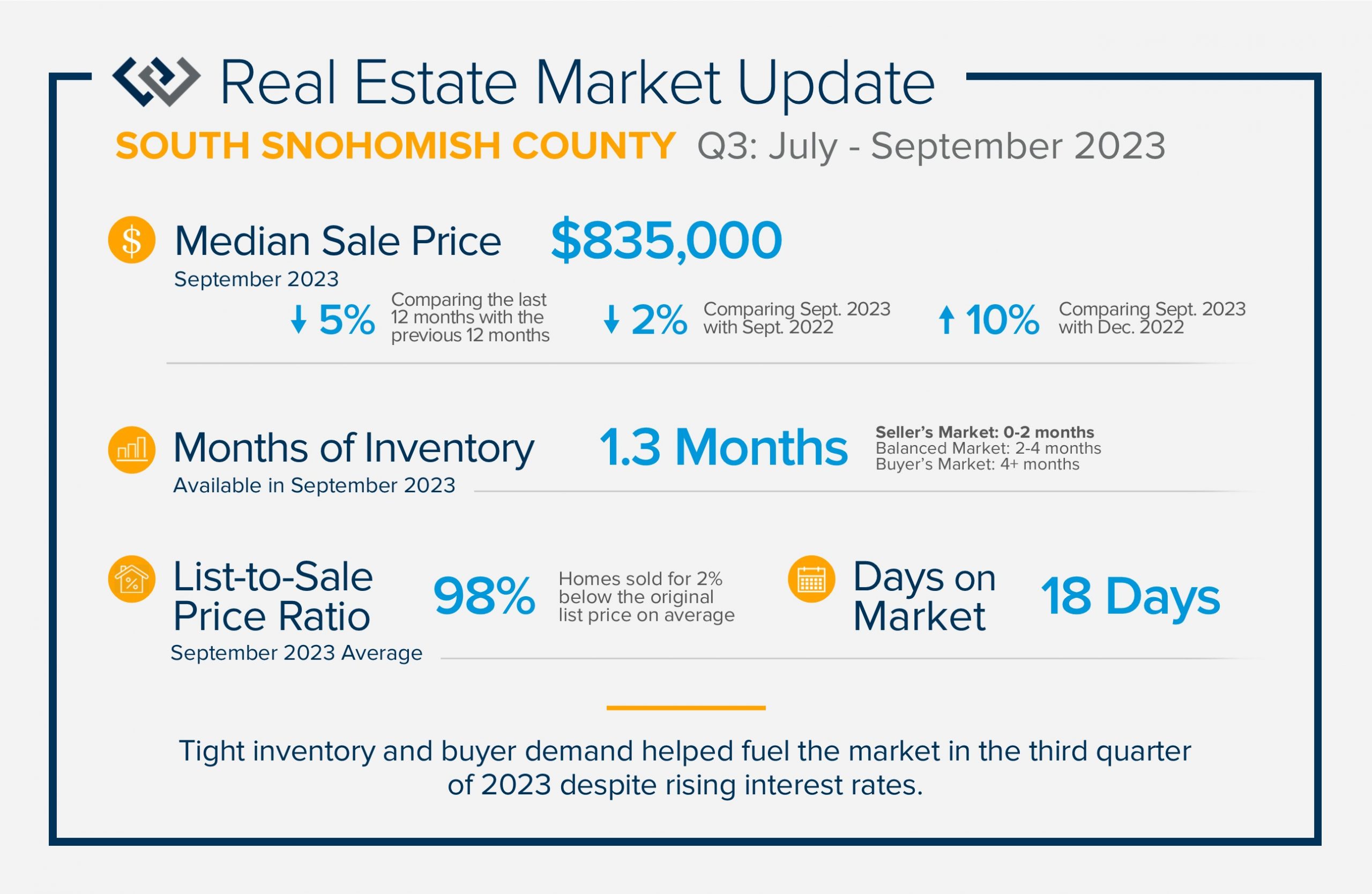

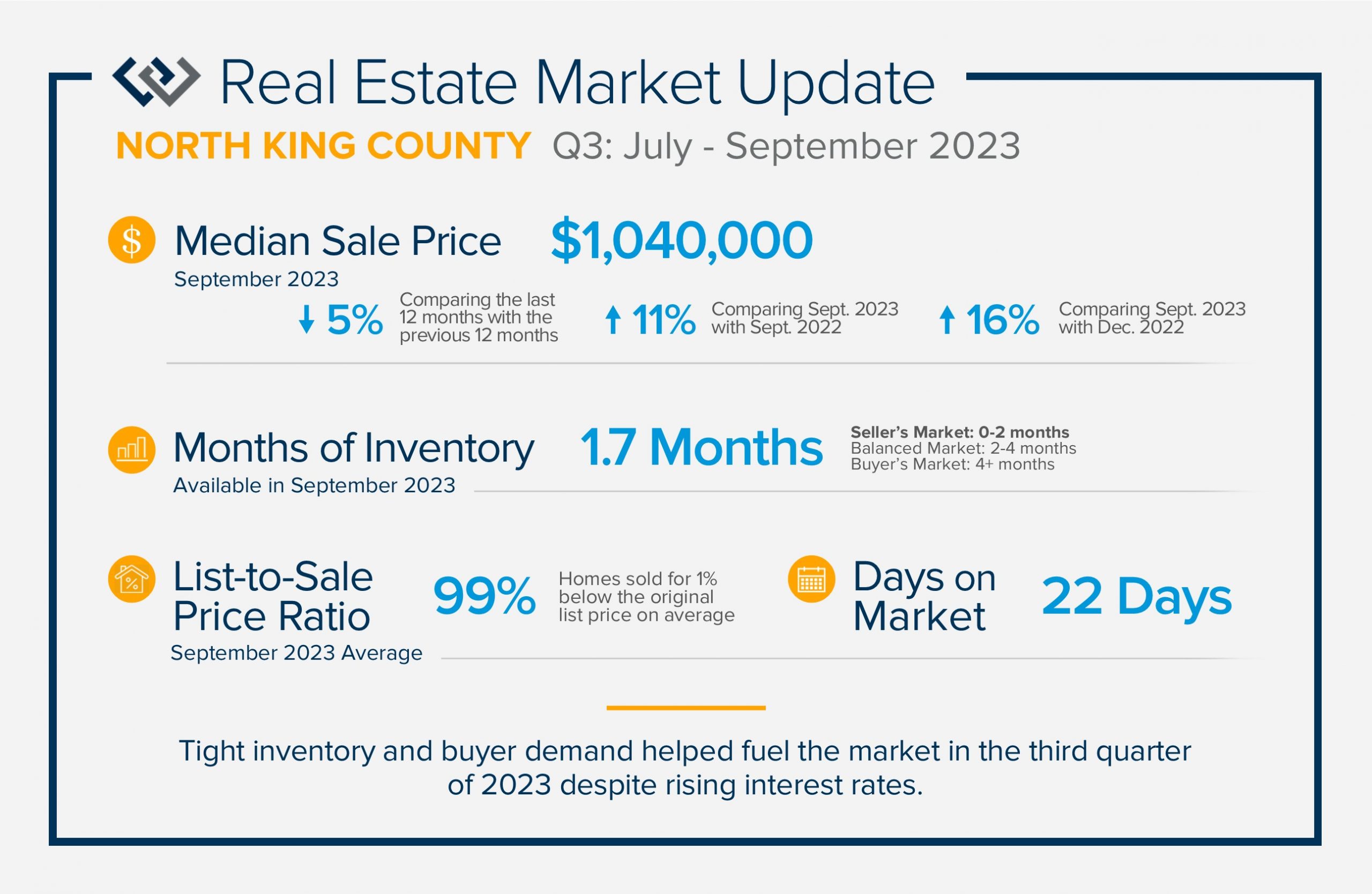

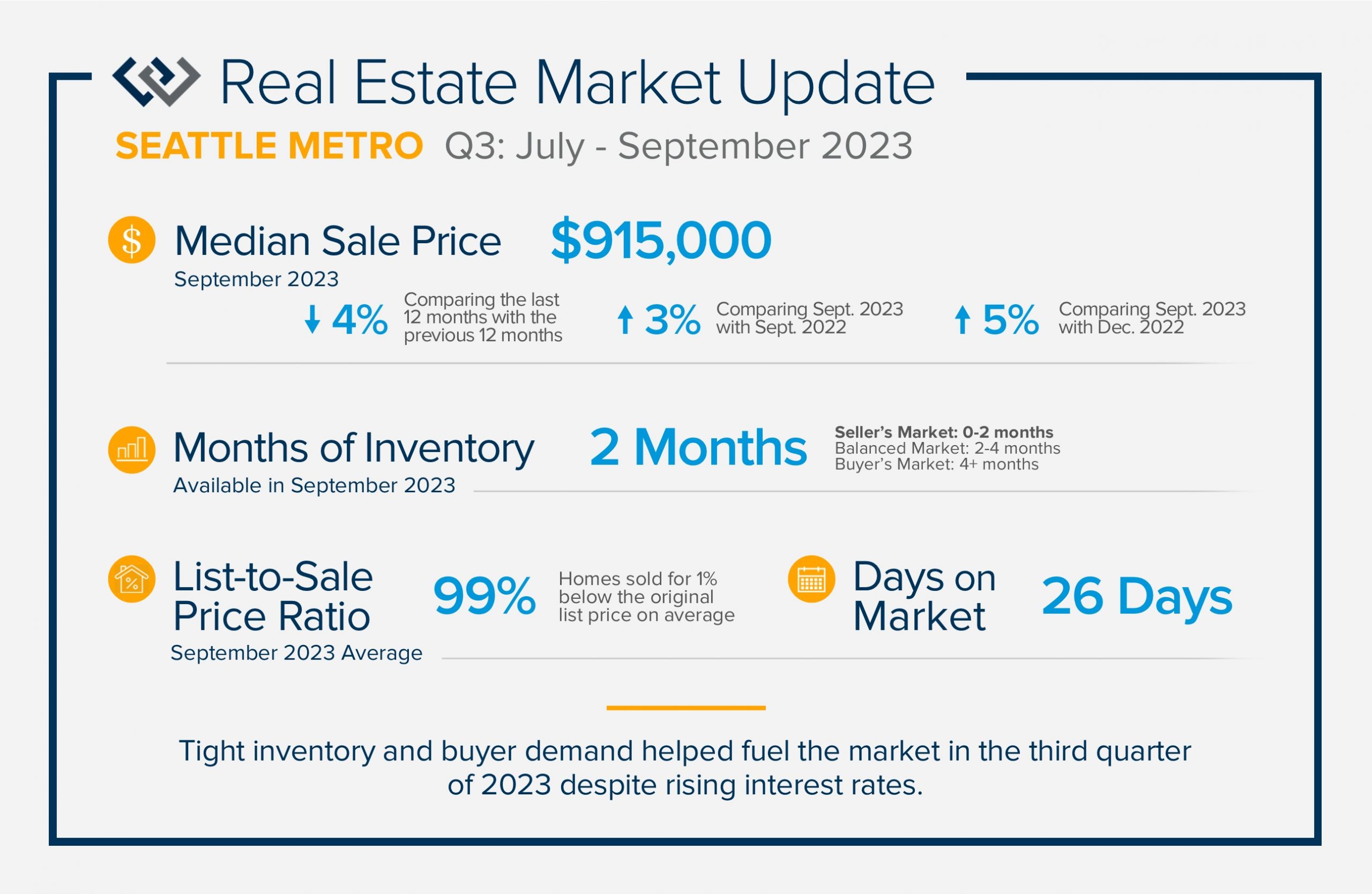

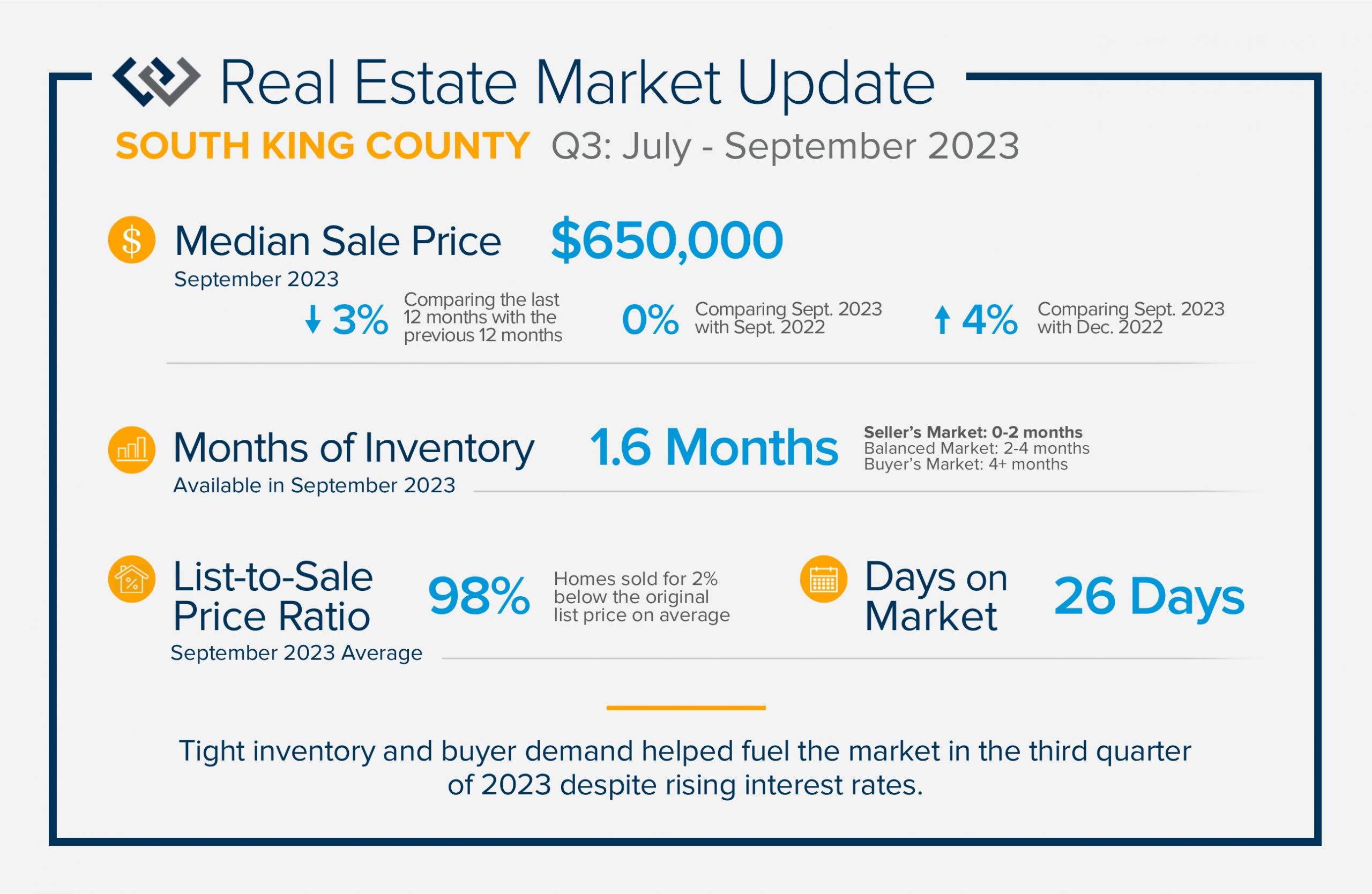

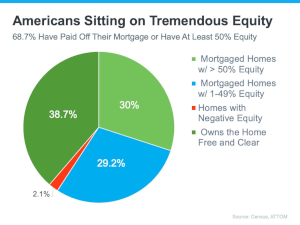

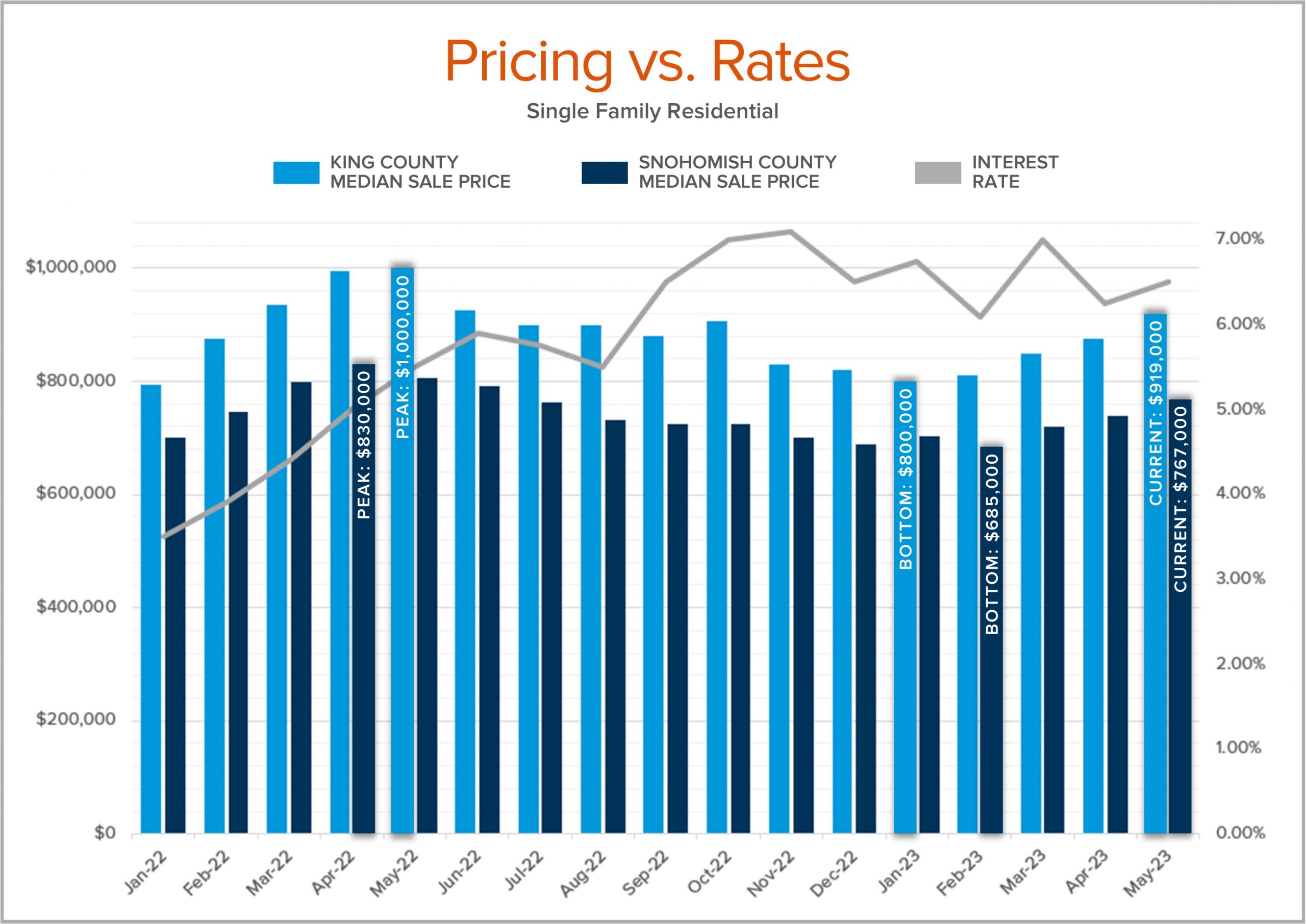

Tight inventory and buyer demand helped fuel the market in the third quarter of 2023 despite rising interest rates. There have been fewer listings in 2023 than in 2022 which has created price growth since the first of the year. Prices peaked in spring 2022, corrected in the second half of 2022, and then they started to rise again in 2023. Home equity is high with over 50% of all homeowners having 50% or more equity in their homes.

Tight inventory and buyer demand helped fuel the market in the third quarter of 2023 despite rising interest rates. There have been fewer listings in 2023 than in 2022 which has created price growth since the first of the year. Prices peaked in spring 2022, corrected in the second half of 2022, and then they started to rise again in 2023. Home equity is high with over 50% of all homeowners having 50% or more equity in their homes.

Most often a home buyer will procure a home loan with a 30-year term and the current interest rate. In the month of August, the 30-year conventional interest rate averaged 7.25%. While 7.25% is reflective of the average over the last 30 years, it is 2-3% higher than what we have experienced over the last 5 years. According to several experts, rates are predicted to decrease as we finish out 2023 and head into 2024. That also means that it is very likely prices will increase when that happens.

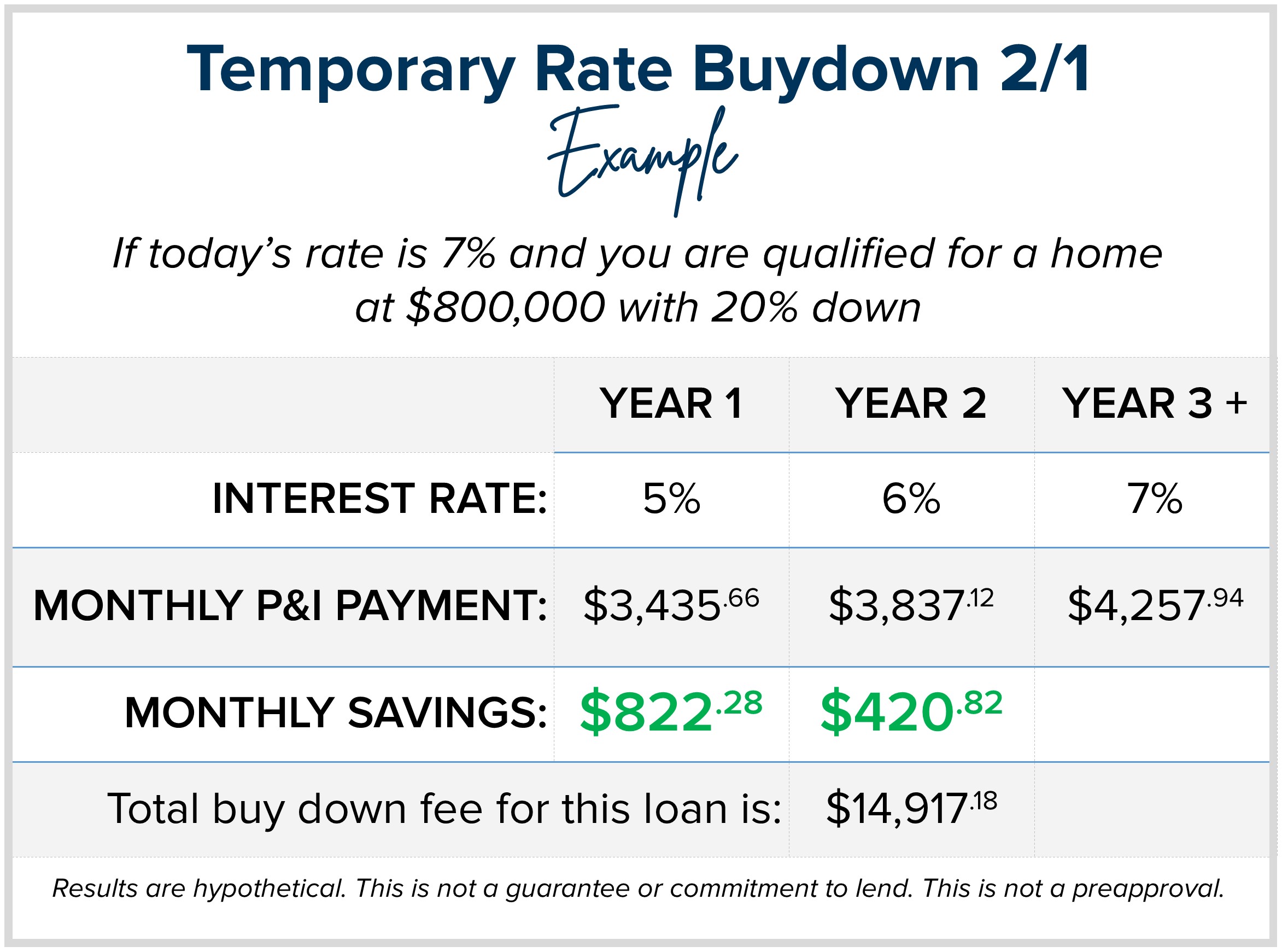

Most often a home buyer will procure a home loan with a 30-year term and the current interest rate. In the month of August, the 30-year conventional interest rate averaged 7.25%. While 7.25% is reflective of the average over the last 30 years, it is 2-3% higher than what we have experienced over the last 5 years. According to several experts, rates are predicted to decrease as we finish out 2023 and head into 2024. That also means that it is very likely prices will increase when that happens. Here is an example, let’s say you are shopping for a house and have the same $800,000 budget and a 20% down payment with today’s rate of 7%. The monthly principal and interest payment would be $4,257.94. You could do a 2-1 buydown (2 points lower in year one and 1 point lower in year 2) which would have your payment in year one be based on an interest rate of 5% with a monthly principal and interest payment of $3,435.66 – a savings of $822.28 a month. For year two, the monthly principal and interest would be based on 6%, resulting in a monthly payment of $3,837.12, a $420.82 savings. The total savings in monthly payments with the 2-1 buy-down over the two years would be $14,917.18.

Here is an example, let’s say you are shopping for a house and have the same $800,000 budget and a 20% down payment with today’s rate of 7%. The monthly principal and interest payment would be $4,257.94. You could do a 2-1 buydown (2 points lower in year one and 1 point lower in year 2) which would have your payment in year one be based on an interest rate of 5% with a monthly principal and interest payment of $3,435.66 – a savings of $822.28 a month. For year two, the monthly principal and interest would be based on 6%, resulting in a monthly payment of $3,837.12, a $420.82 savings. The total savings in monthly payments with the 2-1 buy-down over the two years would be $14,917.18.

Thank you to everyone who pitched in during the Summer Food Drive! Through your generosity, we collectively donated $3,060 and 1,503 pounds of food to Volunteers of America Western Washington food banks! This is all going directly into our communities to help our neighbors in need.

Thank you to everyone who pitched in during the Summer Food Drive! Through your generosity, we collectively donated $3,060 and 1,503 pounds of food to Volunteers of America Western Washington food banks! This is all going directly into our communities to help our neighbors in need.

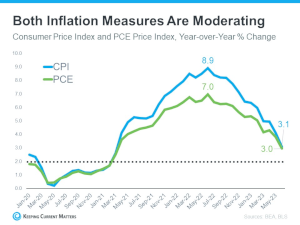

There has always been a direct correlation between interest rates and home prices. The rule of thumb has always been when rates go up prices go down, and vice versa. This was temporarily proven true in the summer of 2022 when rates quickly rose by 2% (3.5%-5.5%) over 5 months. It created a price correction in the second half of 2022 as buyers retreated from the market due to affordability. One should note that price acceleration was rapid from May 2020 to May 2022 and in that two-year period prices grew upward of 50% in King and Snohomish Counties. That was an unsustainable pace. In all honesty, this was inflation’s role in the housing market, and increasing the rates was the Fed’s way of getting control.

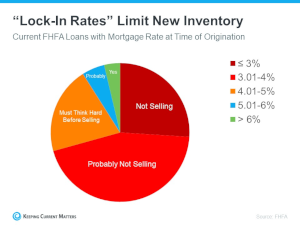

There has always been a direct correlation between interest rates and home prices. The rule of thumb has always been when rates go up prices go down, and vice versa. This was temporarily proven true in the summer of 2022 when rates quickly rose by 2% (3.5%-5.5%) over 5 months. It created a price correction in the second half of 2022 as buyers retreated from the market due to affordability. One should note that price acceleration was rapid from May 2020 to May 2022 and in that two-year period prices grew upward of 50% in King and Snohomish Counties. That was an unsustainable pace. In all honesty, this was inflation’s role in the housing market, and increasing the rates was the Fed’s way of getting control. Believe it or not, the higher rates are keeping prices stable because it is limiting the available inventory for sale. You see, there are plenty of buyers out looking for homes right now, and inventory levels are tight because potential sellers are waiting to make a move because they are holding on to their low rate. Our job market is good, we have people moving to our area and the millennials are out in full force searching for their first homes.

Believe it or not, the higher rates are keeping prices stable because it is limiting the available inventory for sale. You see, there are plenty of buyers out looking for homes right now, and inventory levels are tight because potential sellers are waiting to make a move because they are holding on to their low rate. Our job market is good, we have people moving to our area and the millennials are out in full force searching for their first homes. Here’s the deal though, housing is a reflection of life! According to the US Census, 66% of homeowners would like to upgrade to a nicer home with features that better match their lifestyle, and 45% would like to move to a home to better match the changing size of their household. Life changes motivate moves! Many people are waiting out these life changes until rates come down so they can better afford their desired transition. This has put downward pressure on inventory, limiting selection for buyers, hence creating price growth and stabilization.

Here’s the deal though, housing is a reflection of life! According to the US Census, 66% of homeowners would like to upgrade to a nicer home with features that better match their lifestyle, and 45% would like to move to a home to better match the changing size of their household. Life changes motivate moves! Many people are waiting out these life changes until rates come down so they can better afford their desired transition. This has put downward pressure on inventory, limiting selection for buyers, hence creating price growth and stabilization. We find ourselves in a delicate dance with inflation, rates, inventory, and prices. Someone who desires a move has to consider the impact the rates can have on their payment. Many of these buyers are taking the leap and finding creative ways to offset the rate such as ARM financing, rate buy downs, or they are preparing to re-finance their purchase when rates come down. This way they will have secured a good price which is the basis of their loan.

We find ourselves in a delicate dance with inflation, rates, inventory, and prices. Someone who desires a move has to consider the impact the rates can have on their payment. Many of these buyers are taking the leap and finding creative ways to offset the rate such as ARM financing, rate buy downs, or they are preparing to re-finance their purchase when rates come down. This way they will have secured a good price which is the basis of their loan. Helping people navigate the ever-changing market is a skill, an art, and a calling. I am here for it and find great satisfaction in helping people make big life decisions that help bring joy, solve problems, and make them money! My job is a huge responsibility and it is an honor to serve my clients. If you or someone you know are wondering about how today’s market conditions affect your goals, please reach out. We can dig into the data, assess your dreams and devise a plan.

Helping people navigate the ever-changing market is a skill, an art, and a calling. I am here for it and find great satisfaction in helping people make big life decisions that help bring joy, solve problems, and make them money! My job is a huge responsibility and it is an honor to serve my clients. If you or someone you know are wondering about how today’s market conditions affect your goals, please reach out. We can dig into the data, assess your dreams and devise a plan.

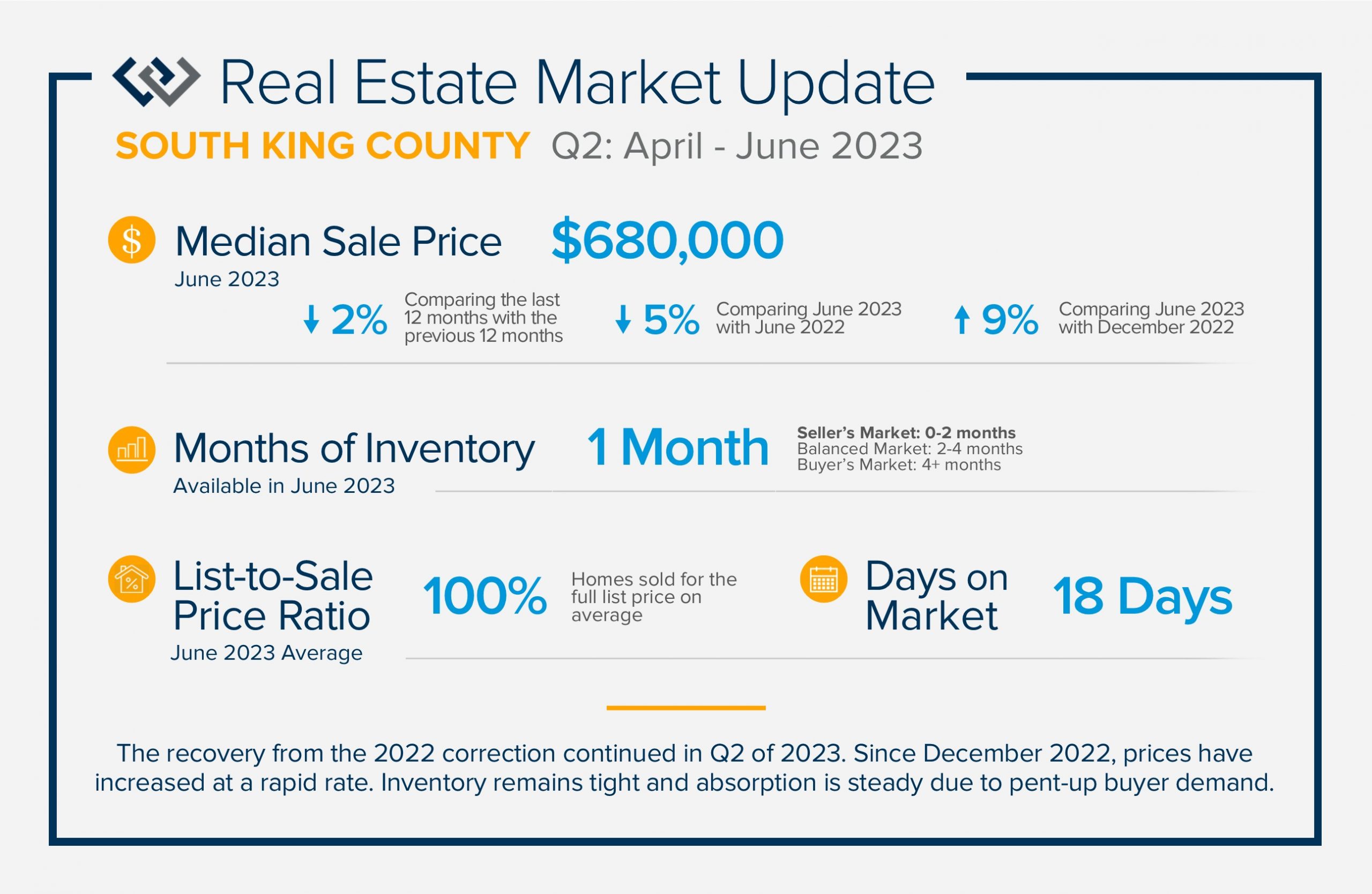

The recovery from the 2022 correction continued in Q2 of 2023. Since December 2022, prices have increased at a rapid rate. Inventory remains tight and absorption is steady due to pent-up buyer demand. Shorter days on market and healthy list-to-sale price ratios illustrate when a seller meets the market with appropriate pricing and is in good condition, a swift and successful sale is in store. Despite higher interest rates the market continues to churn. Rates are anticipated to come down, and when they do competition will increase.

The recovery from the 2022 correction continued in Q2 of 2023. Since December 2022, prices have increased at a rapid rate. Inventory remains tight and absorption is steady due to pent-up buyer demand. Shorter days on market and healthy list-to-sale price ratios illustrate when a seller meets the market with appropriate pricing and is in good condition, a swift and successful sale is in store. Despite higher interest rates the market continues to churn. Rates are anticipated to come down, and when they do competition will increase.

Windermere Community Service Day

Windermere Community Service Day

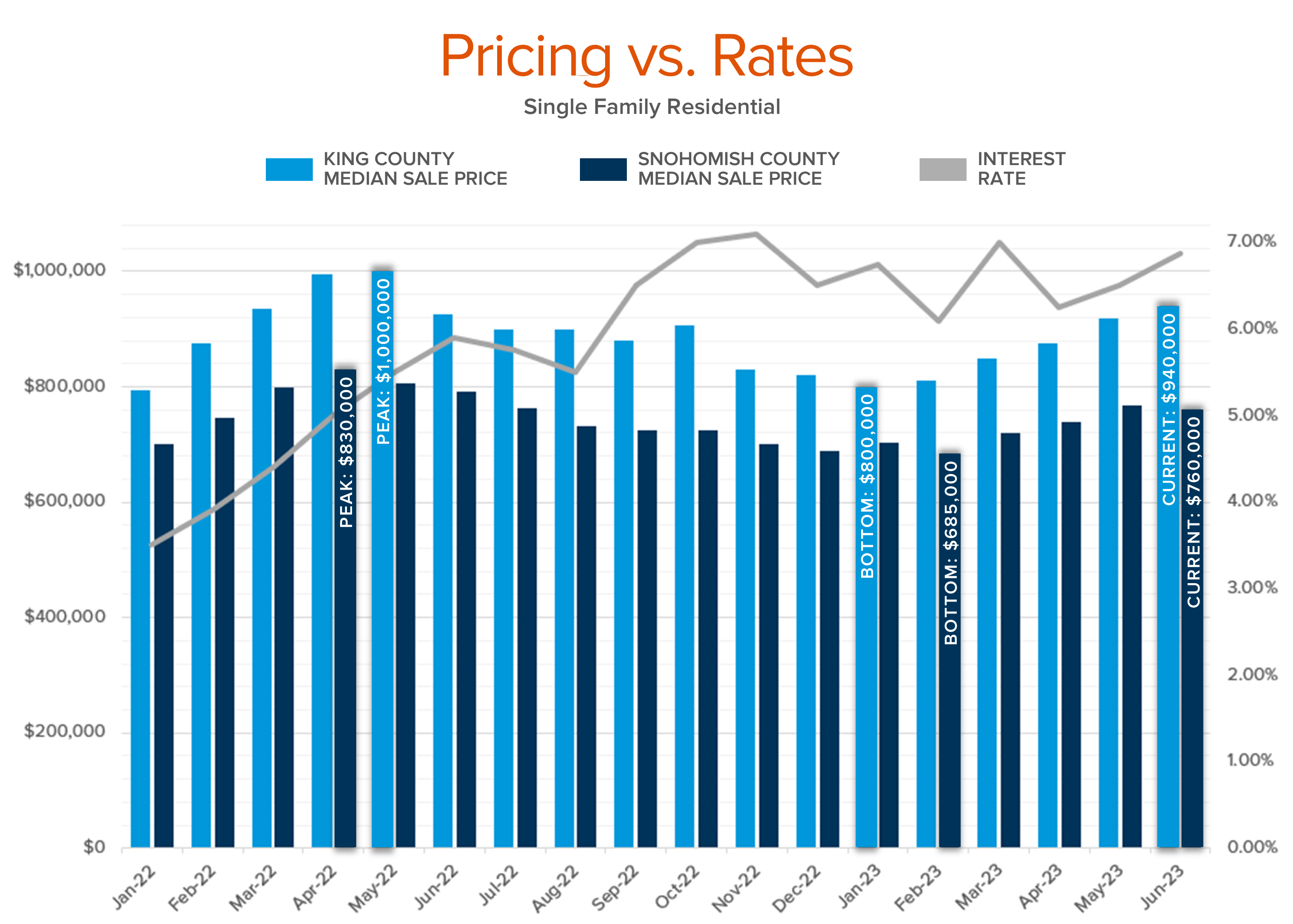

In King County, the median price peaked in May 2022 at $1M and is currently at $919,000 (May 2023), which is down 8% from peak to current. Prices hit bottom in January 2023 at $800,000 which was down 20% (the actual tumble) from the peak but are now up 15% from the bottom!

In King County, the median price peaked in May 2022 at $1M and is currently at $919,000 (May 2023), which is down 8% from peak to current. Prices hit bottom in January 2023 at $800,000 which was down 20% (the actual tumble) from the peak but are now up 15% from the bottom!